Following its latest dividend hike, Waste Management (NYSE:WM) is confidently getting closer to becoming a member of the Dividend Aristocrats — the exclusive club of dividend stocks within the S&P 500 (SPX) that share a remarkable history (25+ years) of annual dividend increases.

Waste Management has already increased its dividend for 20 consecutive years. In the meantime, the company’s irreplaceable role in the industry, management’s optimistic outlook, and improving dividend growth prospects have paved the way for Waste Management to effortlessly ascend to the renowned ranks of this elite group of stocks.

Overall, dividend growth investors are likely to find Waste Management a fruitful option. That said, shares remain relatively overpriced, which could limit the stock’s future upside potential. Accordingly, I am neutral on the stock.

Dividend Growth Powered by Steady Top and Bottom-Line Growth

Waste Management’s prolonged dividend growth streak is being powered by consistently growing revenues and net income, which are, in turn, being supported by the company’s unique qualities. Let’s examine.

Revenue Growth Drivers

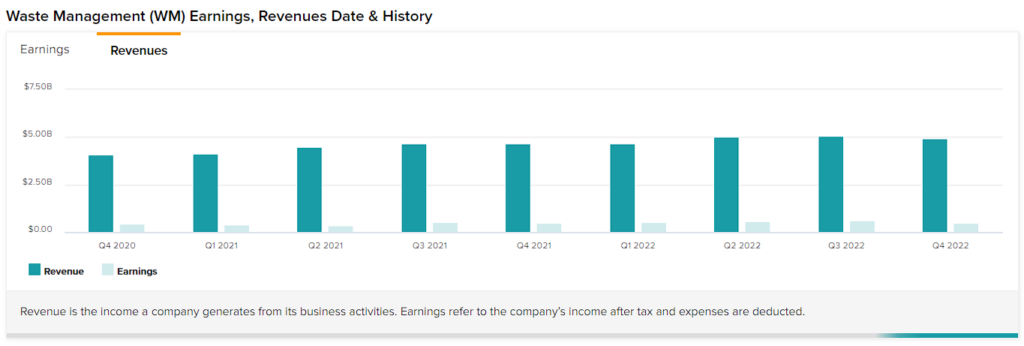

For Fiscal 2022, Waste Management posted revenues of $19.7 billion, up 10% compared to the previous year. Despite the current macroeconomic uncertainties, which impact most industries out there, the company remains unaffected because the waste management industry’s performance is uncorrelated to the overall economy. It’s an essential service that needs to be conducted no matter what, which gives Waste Management fantastic pricing power.

Likewise, as waste volumes increase over time following consistently higher consumption levels, the amount of waste the company has to collect and process tends to increase, also boosting its revenues. These catalysts were the main drivers for the company’s double-digit revenue growth. Specifically, for Fiscal 2022, the company achieved 7.8% higher core pricing while collection and processing volumes rose by 1.3% compared to Fiscal 2021.

Net Income Drivers

In addition to an uptick in revenue, Waste Management’s earnings have been getting a boost from the company’s ability to achieve economies of scale – a wonderful benefit that gradually widens its profit margins, adding even more muscle to its already impressive financial performance.

To understand why this is happening, one must first acknowledge the significant obstacles to entering the waste management industry (i.e., high barriers to entry). It’s not like somebody can start a waste management company and try to compete with the current giants, as this is an oligopolistic space that requires massive capital expenditures.

For context, Waste Management, Republic Services (NYSE: RSG), and municipality-owned firms control more than 75% of the market share in the U.S., while their cash flows are supported by multi-year contracts with governmental entities and corporations.

As a result, Waste management can offer its services with greater efficiency at larger volumes, resulting in improving margins. To quantify this, Waste Management’s operating margin expanded from 14.7% in 2013 to 17.4% in 2022. As one can expect, the combination of higher revenues and expanding margins enables the company to achieve even higher net income growth. In 2022, net income grew by 17.7% to $2.24 billion. Even better, earnings per share jumped by 25.6%, aided by the company’s share buybacks.

Waste Management’s Dividend Growth Potential

As previously noted, Waste Management has an impressive 20-year history of uninterrupted dividend growth, thanks to the company’s astute leveraging of the favorable traits inherent in its industry. The company’s most recent dividend hike took place in February, with management raising the quarterly dividend by 7.7% to $0.70/share.

However, as noted earlier, Waste Management’s earnings per share grew by a much more substantial 25.6% last year, indicating an improving payout ratio. In fact, an improving payout ratio has lately become a trend for the company:

- Fiscal 2020 payout ratio: 62%

- Fiscal 2021 payout ratio: 53%

- Fiscal 2022 payout ratio: 48%

- Fiscal 2023 payout ratio (assumes consensus EPS estimates of $6.00): 47%

Hence, I am confident that Waste Management’s journey toward becoming a Dividend Aristocrat is going to be a smooth one, with no unpleasant surprises — especially given its recession-proof and predictable business model.

Is WM Stock a Buy, According to Analysts?

As far as Wall Street’s sentiment toward Waste Management goes, the stock has a Hold consensus rating based on two Buys and eight Holds assigned in the past three months. At $164.78, the average Waste Management stock price target implies just 6.65% upside potential.

Takeaway — Wall Street’s Sentiment is Likely Right

While I don’t typically align with Wall Street’s perspective, in this particular instance, I must concur that Waste Management is predominantly a Hold at its current price levels. As discussed in this article, Waste Management is a great company, enjoying unique industry tailwinds. Its journey toward becoming a Dividend Aristocrat should further enhance its investment case.

That said, precisely because investors have increasingly appreciated the stock’s qualities in such a volatile environment, shares of Waste Management appear modestly overvalued. At a forward P/E of nearly 26 based on consensus earnings-per-shares estimates for Fiscal 2023, the stock is likely to have little to no upside, moving forward. From an opportunity cost standpoint, with rates on the rise and Waste Management yielding barely 1.8%, the stock is certainly not cheap, despite its strong dividend growth prospects.

That said, it’s worth noting that while waiting for a discount on Waste Management may seem like a wise decision, the stock’s past trend suggests that it may not be a realistic expectation. This is due to the fact that shares have historically traded at a notable premium. It’s an interesting dilemma, nonetheless.