Advertisement

Advertisement

The EUR/USD Daily Technical Analysis for November 20, 2017

By:

The EUR/USD continued to consolidate in a very tight range after surging higher early in the week. Strong housing data appeared to be offset by a

The EUR/USD continued to consolidate in a very tight range after surging higher early in the week. Strong housing data appeared to be offset by a larger than anticipated increase in the Eurozone trade surplus which kept prices range-bound.

Technicals

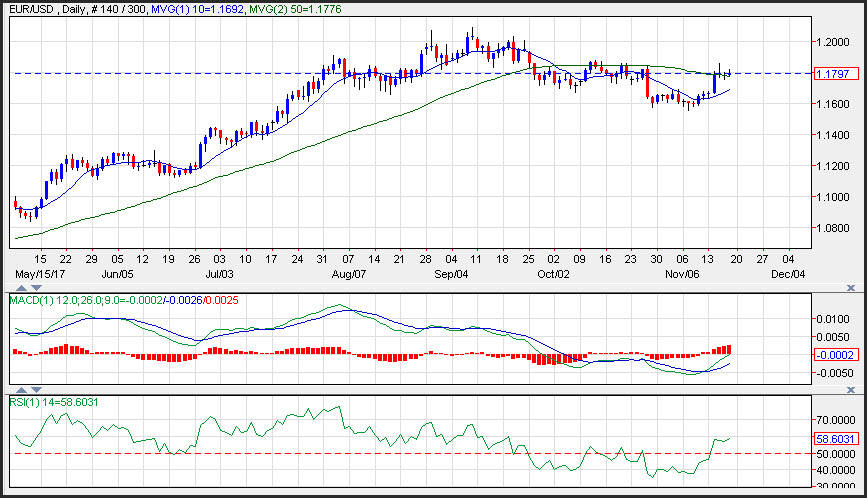

The EUR/USD continued to consolidate after breaking out earlier in the week. The exchange rate is hovering near the 50-day moving average which appear to be acting as a magnate. Support is seen near the 10-day moving average at 1.1692, while resistance is seen near the November highs at 1.1860. Momentum is positive as the MACD (moving average convergence divergence) histogram is printing in the black with an upward sloping trajectory which points to a higher exchange rate.

ECB’s Draghi Say Inflation is not yet self-sustained.

Draghi admitted that the “robust recovery” means the economy “may be becoming more resilient to new shocks”, but stressed that “we still need a patient and persistent approach to monetary policy to ensure that medium-term price stability is achieved”. The ECB President argued that while “we see inflation moving steadily away from the very low levels of recent years”, “progress remains incomplete and partial”, although “as the labor market tightens and uncertainty falls, the relationship between slack and wage growth should begin reasserting itself”. Pretty much a defense of the decision to extend the QE program once again, although with the increasingly optimistic outlook another extension beyond September next year seems very unlikely even if the ECB remains reluctant to commit to an end date for net asset purchases.

The End of ECB QE is Up for Discussion

QE for the ECB is expected to move smoothly until next September and the central bank has not committed to an end date, but comments from Executive Board Member Mersch seem to confirm that in the central scenario there will be no follow-on program when the next QE extension ends in September next year. Indeed, Draghi’s reluctance to officially remove the possibility of another QE extension is likely to have more to do with signaling effects and the ECB’s acute awareness that peripheral markets need the assurance that the ECB is willing to step in again if necessary. Still, a reduction in the ECB’s balance sheet is still far away and the re-investment of redeemed bond holdings will see the central bank propping up peripheral markets well beyond September next year.

Eurozone Trade Surplus Widened

Exports are driving growth in the Eurozone. The Eurozone current account surplus widened in September. The Eurozone posted a current account surplus of EUR 37.8 billion in September, up from EUR 34.5 billion in the previous month, leaving the 3 months rate on an upward trend as the goods surplus continues to widen. This is consistent with indications that net exports underpinned overall growth in the third quarter of the year.

The unadjusted financial account showed direct and portfolio investment inflows of EUR 57.9 billion, down markedly from the EUR 85.4 billion in the previous month, with portfolio investment falling sharply amid outflows of equity investments. Accumulated data for the 12 months to September show total direct and portfolio investments of EUR 414.9 billion, down from EUR 670.7 billion in the 12 months to September last year.

The Fed’s Kaplan Said Balance Sheet Unwind is Necessary

Dallas Fed’s Kaplan said the balance sheet unwinding began when the Fed thought it was unlikely to return to zero interest rates and he’s confident in economic growth, since household leverage has fallen, expecting 2% plus growth next year. Kaplan expects more slack to come out of the labor sector, but if the unemployment rate rises that could be a sign of impending recession. He said Powell as chairman represents continuity, though others like Quarles may bring new ideas. He endorses reviewing Fed governance, frameworks, targets and small bank supervision, as any organization needs to make changes.

U.S housing starts surged 13.7% to 1.290 million in October, more than erasing the 3.2% hurricane-related September drop to 1.135 million which was revised from 1.127 million. Building permits rose 5.9% to 1.297million from a revised 3.7% drop to 1.225 million which was 1.215 million. As for some particulars, single family starts bounced 5.3% after the prior 4.4% drop which was revised from -4.6%, while multi-family starts rocketed 36.8% higher following the prior 0.3% gain which was revised from -5.1%. Housing completions increased 12.6% to 1.232 million.

About the Author

David Beckerauthor

David Becker focuses his attention on various consulting and portfolio management activities at Fortuity LLC, where he currently provides oversight for a multimillion-dollar portfolio consisting of commodities, debt, equities, real estate, and more.

Did you find this article useful?

Latest news and analysis

Advertisement