Cimarex Energy Co (XEC): Time For A Financial Health Check

A market capitalization of USD $10.99B puts Cimarex Energy Co (NYSE:XEC) in the basket of stocks categorized as large-caps. These stocks draw significant attention from the investing community due to its size and liquidity. However, a more fundamental aspect of investing in large caps is its financial health. Why is it important? A major downturn in the energy industry has resulted in over 150 companies going bankrupt and has put more than 100 on the verge of a collapse, primarily due to excessive debt. Here are few basic financial health checks to judge whether a company fits the bill or there is an additional risk which you should consider before taking the plunge. View our latest analysis for Cimarex Energy

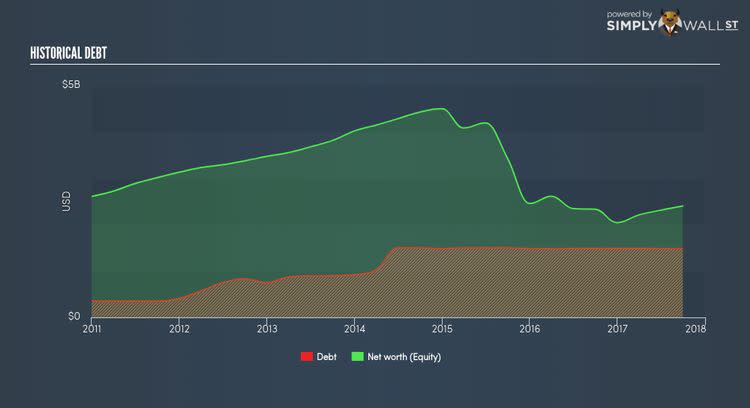

Can XEC service its debt comfortably?

Debt-to-equity ratio standards differ between industries, as some some are more capital-intensive than others, meaning they need more capital to carry out core operations. A ratio below 40% for large-cap stocks is considered as financially healthy, as a rule of thumb. For XEC, the debt-to-equity ratio is 61.88%, which means, while the company’s debt could pose a problem for its earnings stability, it is not at an alarmingly high level yet. We can test if XEC’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings should cover interest by at least three times, therefore reducing concerns when profit is highly volatile. XEC’s profits amply covers interest at 12.02 times, which is seen as relatively safe. Lenders may be less hesitant to lend out more funding as XEC’s high interest coverage is seen as responsible and safe practice.

How does XEC’s operating cash flow stack up against its debt?

A simple way to determine whether the company has put debt into good use is to look at its operating cash flow against its debt obligation. This is also a test for whether XEC has the ability to repay its debt with cash from its business, which is less of a concern for large companies. In the case of XEC, operating cash flow turned out to be 0.62x its debt level over the past twelve months. This is a good sign, as over half of XEC’s near term debt can be covered by its day-to-day cash income, which reduces its riskiness to its debtholders.

Next Steps:

Are you a shareholder? XEC’s high cash coverage means that, although its debt levels are high, investors shouldn’t panic since the company is able to utilise its borrowings efficiently in order to generate cash flow. Since XEC’s financial position may differ over time, I encourage assessing market expectations for XEC’s future growth on our free analysis platform.

Are you a potential investor? Although understanding the serviceability of debt is important when evaluating which companies are viable investments, it shouldn’t be the deciding factor. After all, debt financing is an important source of funding for companies seeking to grow through new projects and investments. As for next steps, You should continue to assess XEC’s Return on Capital Employed (ROCE) in order to see management’s track record at deploying funds in high-returning projects.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.