Advertisement

Advertisement

Natural Gas Price Analysis for February 20, 2018

By:

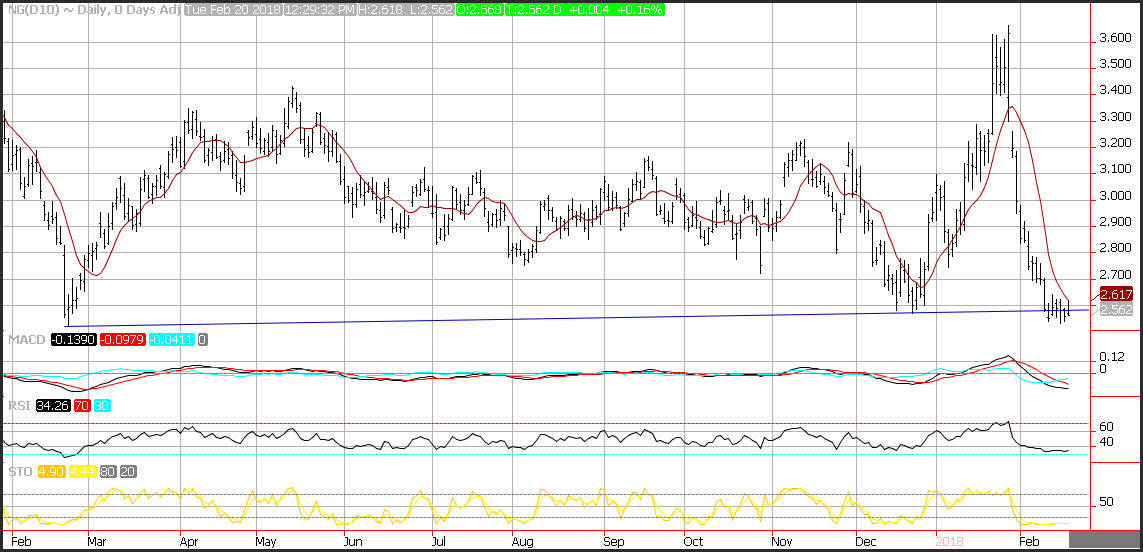

Natural gas prices continue to consolidate after tumbling down to support level near the 2.50 region. Warmer than normal weather is forecast to cover the

Natural gas prices continue to consolidate after tumbling down to support level near the 2.50 region. Warmer than normal weather is forecast to cover the eastern portion of the United States, but a new cold ridge is forming from the west which could keep prices from falling further. Last week’s inventory report showed that stocks continue to decline which could be a function of stronger than expected exports of liquefied natural gas. Prices attempted to pierce through the 10-day moving average at 2.167 but were unsuccessful. Support is seen near the recent February lows at 2.53. Negative momentum is beginning to decelerate as the MACD (moving average convergence divergence) histogram prints in the red with a climbing trajectory which points to consolidation. The fast stochastic is oversold, and points to a potential rebound. The current reading of 4, is well below the oversold trigger level of 20 and could foreshadow a correction.

Exports Surge

The U.S. trade price report beat estimates with strength in core prices and ex-agricultural export prices in particular, alongside the expected big gain in oil import prices, though with a downtick for food export prices. Price gains in recent years have been skewed toward exports. The trade price data, alongside January strength in the CPI, PPI and hourly earnings data, add to the narrative of rising inflation, though we read little into these concurrent gains beyond the uptrend in most year over year price pressures into mid-year due to hard comparisons.

More generally, trade price firmness since 2016 has been led by a drop in the dollar and recovering growth abroad, and we now face an upgrade in U.S. growth prospects with the new tax and budget laws. Production restraint from OPEC and December supply disruptions lifted oil prices into January, though soaring U.S. shale output has depressed petroleum prices into February as the U.S. fills the OPEC void. Export prices ex-agriculture and import prices ex-petroleum are poised for respective gains in 2018 of 4% and 3%, following respective gains of 2.7% and 1.3% in 2017 and 1.4% and 0.3% in 2016.

About the Author

David Beckerauthor

David Becker focuses his attention on various consulting and portfolio management activities at Fortuity LLC, where he currently provides oversight for a multimillion-dollar portfolio consisting of commodities, debt, equities, real estate, and more.

Did you find this article useful?

Latest news and analysis

Advertisement