A day before Diwali and on the last day of Samvat 2074, here's a look at the stock recommendations by Epic Research and Way2Wealth, which are likely to be the best picks for Samvat 2075.

Recommendations by Epic Research

Bajaj Auto

The firm is an automobile major that has been in a long upward trend since early 2011. We like to continue to be with the trend and take advantage of its upside momentum at favorable levels which is giving a decent risk reward opportunity in short term to medium term. Stock is trading at 2670 - 2650 levels and is well supported by long standing support trendline drawn from troughs of 2011. Two Leading indicators, such as Momentum and RSI are giving a bullish divergence. The Automobile as a sector leads the price action in a trending scenario and we expect Bajaj Auto to resume its long standing uptrend from current levels.

We recommend to accumulate Bajaj Auto in the range of 2600 - 2630 for an Upside target of 3100 on medium term basis. Stop loss for the trend trade will be 2470 on closing basis.

Alternate Scenario - Buy Above 2700 on closing basis: Target 3100 - 3150 Stop loss - 2550.

LT Foods

A long declining trend or a due correction seems to be nearing its pattern as stock has taken a very good support at recent support levels of 35 - 38 levels. A very bullish trend has seen a due correction with stock declining around 66% and retracing back on higher timeframes.

A Pullback is seen from a long standing trendline drawn from troughs of early 2015, a crucial low for its overall bullish trend. We expect this to be a short term bottom while a sustained move can stretch the trend to a much higher levels.

We Recommend to accumulate LT Foods/ Daawat in the range of 40 - 35 for an upside Target of 58 - 65 in medium term perspective. Stop loss can be placed at 32 on closing basis.

Alternative Scenario - Buy on declines.

TVS Motor

It has seen a classic correction in a long established bullish trend. On a higher timeframe it is a due correction that seems to be over in near term with stock sustaining at lower levels which are its long term support. A support trendline drawn from troughs of 2013 can be seen

giving a strong support at 520 levels which also coincide with its Fibonacci retracement. Multiple confluences at these zones suggest an impending up move can be seen in stock with an upside momentum to its previous swing high in short term. Leading indicators suggest anreversal with positive divergence as well.

We Recommend to accumulate TVS Motor on dips in the range of 540 -520 with an upside target of 600 - 640. Stop loss can be placed at 500 on closing basis.

Alternative Scenario - Buy on Dips

UPL Ltd

It is one of the outperforming stocks suited for portfolio which needs to be churned for a higher return. Stock is in its own secular uptrend since 2013 making higher tops and higher bottoms with a minor consolidation, which are bullish continuation pattern on higher timeframe.

A recent decline gives us an opportunity to enter into the uptrend with a favorable risk reward at current levels.

We recommend to accumulate UPL Ltd on declines in a range of 700 - 670 for a medium term perspective with upside target of 820 - 1040.

Alternative Scenario - A long term positional trade can be initiated at current levels of 700 - 710 in small quantity with Stop loss at 650 for an upside target of 1000 plus.

Adani Power

Stock has been in a consolidation range since 2013 - 2018 while on a recent higher timeframe it has given a breakout from long standing resistance line drawn from peaks of 2014. The breakout seems evident looking at leading indicators such as RSI which now seems to indicating a trending scenario. Volume Weighted indicators suggest a increased buying momentum as well.

Alternate Scenario - Buy above 52.75 on closing basis with Target of 63 Stop loss - 45.

Recommendations by Way2 Wealth

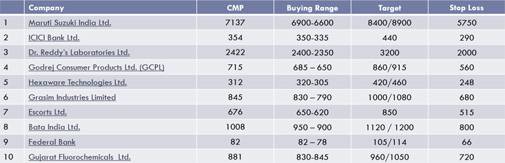

Maruti Suzuki

At current market price of Rs 7,137, Maruti Suzuki is currently trading at an FY20E P/E of 19.1. All business parameters such as industry consolidation, market share improvement, reduced JPY exposure and improving the share of premium products have improved MSIL's position immensely. We see headroom for re-rating of the stock from current levels. Target 8,400-8,900 with stop loss of 5750.

ICICI Bank

At CMP of Rs 354, ICICI Bank trades at a FY19E and FY20E P/B of 2.12 and 1.91 respectively. ICICI Bank is in the midst of an improvement in the operating environment (stressed asset resolution and growth pick up) and is showing healthy signs of earnings normalization. With challenges relating to the management transition getting addressed the focus of the banks is now to grow core operating profits. We expect the bank to deliver an all-around improvement in asset quality, growth, and margins over the next few years. We advocate the investor to start accumulating this stock in a range of 350 to 335 with a price target of 440. Stop loss should be placed below 290.

Dr Reddy's Laboratories

At the current market price of Rs 2,422, Dr Reddy trades at a PE of 25x FY19E and 19xFY 20E respectively. We expect key large complex drug ANDA approval/launch in the US,benefit from portfolio rationalization and news flow on facility inspection to be key triggers for the company. Risks to our investment idea includes any regulatory issues, delays in product launches in the US, and adverse foreign exchange fluctuations. We believe that stock has potential to rally higher and advocate investor to buy this counter in a range of 2400 to 2350 with an up side target of 3200. Stop loss should be placed below 2000.

Godrej Consumer Products

GCPL is on a firm footing going forward given the 1) resurgence of domestic FMCG demand with rural demand expected to outpace urban demand 2) improved management focus on growing the international business portfolio while improving EBITDA margins to mid -teens over the next 3 years 3) series of new launches led by innovation envisaged over the FY18-20E period to result in robust market share gains ultimately driving top line growth.

Apart from a reputed parentage, strong brands and a legacy of market outperformance over the last decade, GPCL has a strong balance sheet (FY 18 D/E of 0.4x), healthy dividend payout policy, negative working capital cycle, and a robust 25% plus core return ratio profile. Based on Bloomberg consensus estimate, GCPL is expected to deliver sales, EBITDA and PAT CAGR of 13%, 16.7%, and 18.8% respectively over FY18-20E. At CMP, of Rs 715, the stock is trading at a P/E of 36.2x FY20E EPS. Investors are adviced to buy this stock in a range of 685 - 650 with a price target of 860/915. Stop loss should be placed below 560.

Hexaware Technologies

According to consensus Bloomberg estimates the company is well positioned to continue on its double digit growth path with sales, EBITDA and PAT to grow at a CAGR of 16. 2%, 15. 6% and 15. 6% respectively over CY 17-19E. Management commentary suggests, that Europe business will continue to maintain a healthy growth trajectory while A PAC is expected to contribute positively from Q4CY 18 onwards. The RIMS portfolio that contribute 12% of overall revenues will continue to lead the growth over CY 17-19E (achieved 46% CAGR over last 8 quarters) However, the stricter visa norms in the US continue to put pressure on margins over the short term. Post the sharp correction recently, the stock is trading at 12. 5x CY 20E EPS which is at a discount to its peers. We advise investors to start accumulating this stock. At current levels or at any dip.

Grasim Industries

At the current market cap of Rs 55, 780 cr, the implied cumulative value of Grasim's long -term holdings in Ultratech Cement (UTCL), Aditya Birla Capital (ABCL) (45% holding company discount) and other group investments (50% holding company discount) stood at Rs 43,518 crore. As a result, the standalone entity is trading at inexpensive valuations on a TTM basis at a P/E of 5.4x and an EV/EBITDA of 3.1x. Therefore, we are POSITIVE on the stock given the improved operational performance and the aggressive expansion plans that are expected to drive robust and sustainable profitability growth going forward. We believe that the downside in this stock is limited and investors can use this dip as an opportunity to accumulate this stock.

Escorts Ltd

Escorts earnings growth of 23% over FY18-20E would be largely driven by 11% volume CAGR in its tractor business over FY18-20E and steady EBITDA margin expansion of 100bps over the next 2 years. With surplus capacities across segments, Escorts has limited capex needs leading to strong FCF generation and healthy return ratios over the next 2 years. At CMP of Rs 676, Escorts is currently trading at an FY20E PE and EV/EBITDA of 11.5 (adjusted for treasury stock) and 9.7 respectively. We recommend investors to buy this stock in a range of 650 to 620 with an upside price target of 850. Stop loss should be placed at 515.

Bata India

Going forward, Bata is firmly placed to strike a fine balance between volume growth and margin expansion given its large retail network, series of new launches, established premium brands and increased advertisement spends. Furthermore, the recent increase in threshold limit from Rs 500 to Rs 1000 for levying 5% GST rate augurs well for Bata given its current blended realization of Rs 560/pair. All these initiatives taken by the company would help them deliver sales, EBITDA and PAT CAGR of 11%, 18.7%, and 20.8% respectively over FY18-20E.

The company apart from its debt -free status has an extremely efficient business model with a negative working capital cycle of 40 days and with the premiumization strategy unfolding we expect its RoCE to stay elevated above 20% levels. At the CMP of Rs 1, 008, Bata trades at 39x FY20E EPS but given the robust growth prospects, strong parentage and excellent brand recall the company can continue to command premium valuation as it has in the past. We advise investor to accumulate this stock in a range of 950 - 900 with a price target of 1120 and in case of further optimism stock likely to rally till 1200. Stop loss should be placed below 800 and any break below 800 will negate our bullish view.

Federal Bank

At CMP of Rs 82, Federal Bank trades at an FY19E and FY20E P/B of 1.2x and 1.1x respectively as per Bloomberg consensus estimates. Federal Bank delivered a strong operational performance at a time that appeared challenging on account of Kerala floods and continued cleansing of the balance sheet. The Bank has maintained healthy levels of business growth and is well positioned to gain market share in both corporate and retail segments. Management has sounded confident to maintain gross slippages at Rs 14-15 billion for FY19 and aims to deliver an exit ROA of 1%.

We advise investor to buy Federal Bank at current level of 82 and add more on dips to 78 for an upside price target of 105/114. Stop loss for this trade should be placed below 66.

Gujarat Fluorochemicals

At the current market cap of Rs 9,732 Cr, the implied cumulative value of GFL's long -term holdings in Inox Wind (57.0%), Inox Leisure (48. 1%) and other investments after applying a 45% holding company discount stood at Rs 1, 325.

As a result, based on FY20E Bloomberg consensus estimates the standalone entity is trading at 16. 5x P/E and 10. 7x implied P/E and EV/EBITDA multiples respectively. Operational performance at GFL has improved robustly with EBITDA margins at 31% in Q1FY 19 (22% in Q1FY 18) thereby resulting in an EBITDA of Rs 213 Cr. Therefore, we are POSITIVE on the stock as it depicts all the qualities of a turnaround candidate such as its advent into VAP streams, improving return ratios profile, low debt levels, ADD protection ($2637 /MT on PTFE imports from China that are valid for a period of five years till July 2022) & further amplified by favorable global scenario.

This stock can be bought on minor dips around the above mentioned supports of 830 levels. While, the stop loss are seen around 720 levels.

Copyright©2024 Living Media India Limited. For reprint rights: Syndications Today