The Wall Street conference calendar is heating up, and Deutsche Bank just completed its annual DB Tech Conference in Las Vegas.

At the conference, 5-star Deutsche Bank analyst Ross Seymore met Qualcomm (QCOM) president Cristiano Amon to discuss the company’s ongoing legal woes, market dynamics, and most importantly, the company’s vision for the future of 5G.

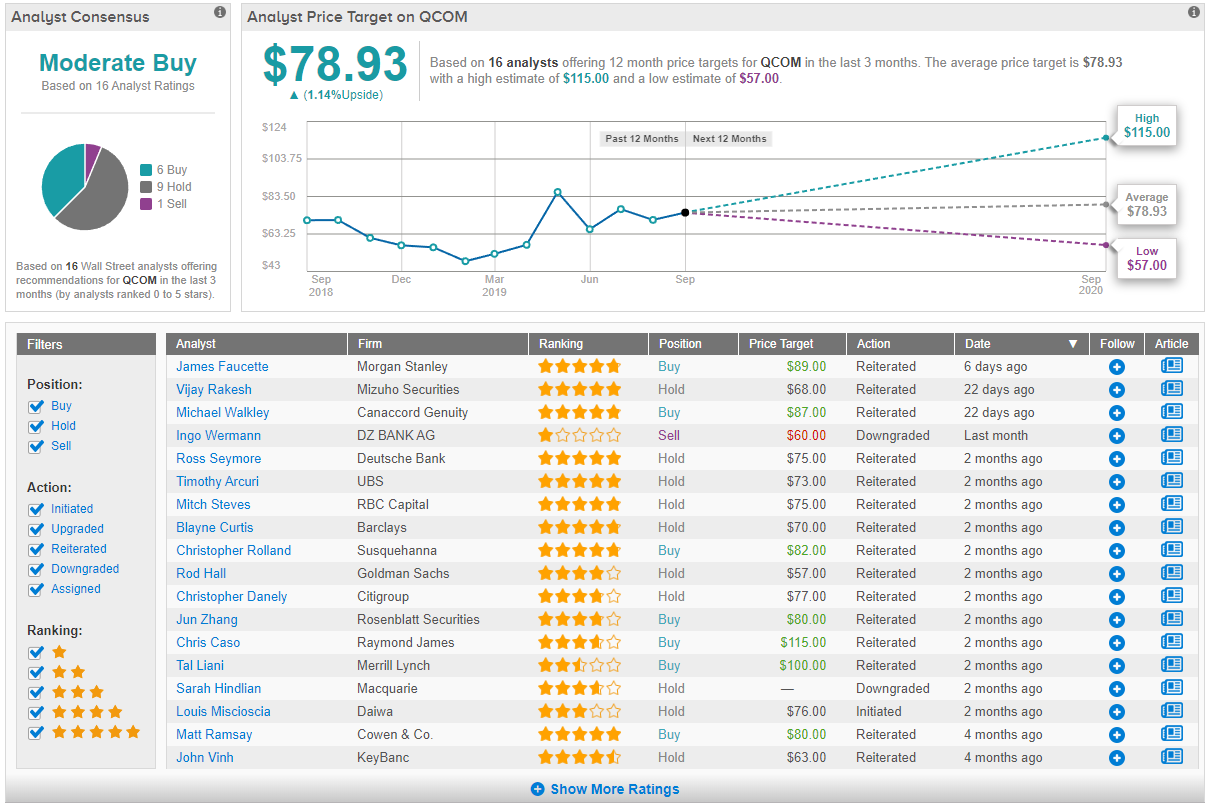

Overall, Seymore remains sidelined on QCOM stock with a ‘hold’ rating and $75 price target, which implies a slight downside to Monday’s $78.04 close.

As always, we like to give credit where credit is due. According to TipRanks, which measures analysts’ and bloggers’ success rate based on how their calls perform, Seymore has earned a yearly average return of 26.6% with an 82% success rate. Notably, Seymore is ranked #17 out of 5,551 analysts.

Qualcomm has recently won a partial stay against the enforcement of a sweeping antitrust ruling in a lawsuit brought by the FTC. Oral arguments are scheduled for January, with potential resolution in the Ninth Circuit by mid 2020, though “Court timelines could change at anytime,” Seymore noted. On the recent 5-year direct worldwide patent license agreement signed with LGE, Seymore says “the company pointed to the new royalty-bearing agreement as a proofpoint to the stability of its QTL business.”

Apart from the legal matters, Qualcomm stock has been hit by macro/trade headwinds, channel inventory reduction (especially in China), lengthening replacement cycles in a mature market, and consumer pause ahead of 5G device launches. Seymore points out that “Qualcomm expects the softness to remain through the rest of the calendar year, with both revenue and earnings to stay in a similar range in 2H CY19 (DBe F4Q19/F1Q20 revs of $4.70b/$4.69b, PF EPS of $0.71/$0.72 respectively).”

Furthermore, by the first calendar quarter of 2020, the company anticipates reaching an inflection point with the launch of 5G technology. The company sees 5G as a significant opportunity for Qualcomm to grow its chip business amidst economic concerns and slowdown in sales. Seymore commented, “We continue to believe QCOM is well positioned for a leadership position in 5G on increasing dollar content opportunity (~1.5x 4G levels) and the co’s early traction on 5G design wins (150+ launched or in development) with a high RF-attach rate.”

All in all, the Street largely seems to echo Seymore’s neutral sentiment. Out of 16 analysts polled by TipRanks in the last 3 months, 6 are bullish on QCOM stock, 9 remain sidelined, and only one is bearish on the stock. The average target price among these analysts stands at $78.93, suggesting the stock price is fairly valued with limited upside ahead.