The storied City of London was once the center of global finance, and while that title has passed to Wall Street, London remains the headquarters for some of the world’s largest banks and investment firms. Barclays, first established in the goldsmith business in 1690, is one of these. Today is a major conglomerate and a powerful name in the global banking industry.

Barclays is ranked 12 out of 50 in the TipRanks database of major investment research firms. At last count, the bank supported a cadre of 256 financial analysts and investment experts, whose 12,000 combined recommendations have a 58% success rate and a 6.1% average return.

So, let’s take a look at three Buy stocks which Barclays analysts have recently given a thumbs up:

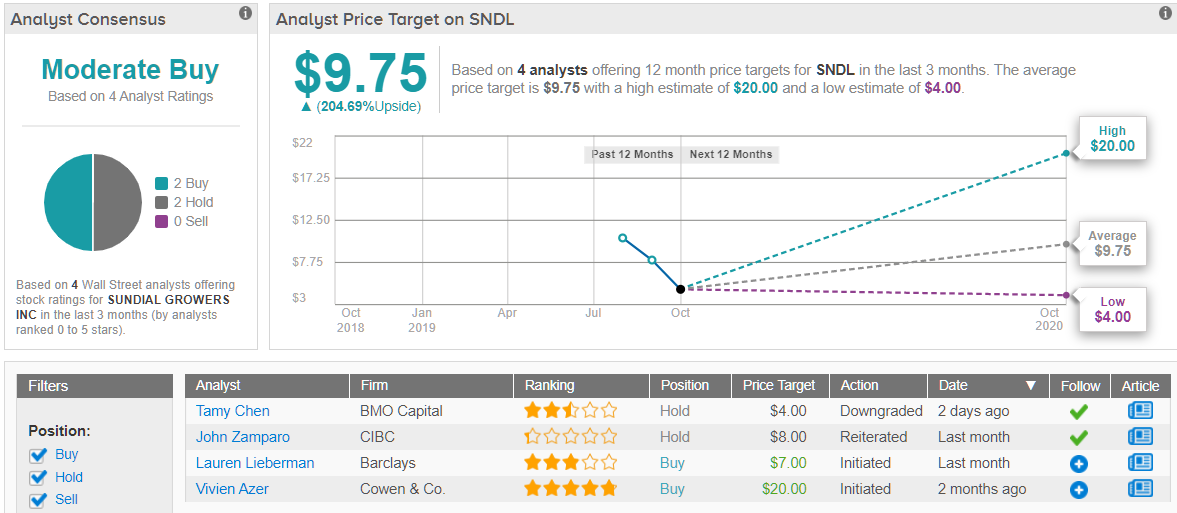

Sundial Growers (SNDL)

Canada’s recently legalized cannabis industry has already brought a series of mid- to large-cap producers to investors’ attention, but the new market is also a fertile ground for start-up players. Sundial is a new company, based in Alberta, where it produces a several lines of high-quality lines of cannabis for the recreational and wellness markets.

The company plays its ‘Alberta heartland’ origin for an asset, boasting that it combines ‘tried-and-true heartland farming with innovative horticultural techniques’ in its production operations. Where many of Canada’s cannabis companies aim for mass or large-scale production in the grow houses, Sundial focuses on producing a consistent, pure strain that customers will find reliable.

Sundial’s focus on product quality over rapid growth has put it in on a faster path toward profitability, in an industry where most of Canada’s cannabis companies operate in the red. Sundial’s overhead is among the lowest of its peers, with operating expenses rated at 50% of total sales compared to an sector average of 171%.

Barclays’ Lauren Lieberman is bullish on Sundial in the volatile Canadian cannabis sector. She says, “The company can set itself apart from peers given a focus on profitable growth. Sundial is already nearly profitable in its Canadian home market, and its acquisition of Bridge Farm should enable the company to ultimately become a low-cost mass-scale producer of CBD products.” Her price target, $7, represents a 107% upside potential for the stock. (To watch Lieberman’s track record, click here)

Overall, Sundial is considered a Moderate Buy from the analyst consensus, based on 2 Buys and 2 Holds. The stock only IPOd in July of this year, and was considered overvalued at that time; shares have fallen from an August peak of $13 to the current $3.25. The average price target now, however, is $9.75, suggesting room for a 200% upside. (See Sundial Growers stock analysis on TipRanks)

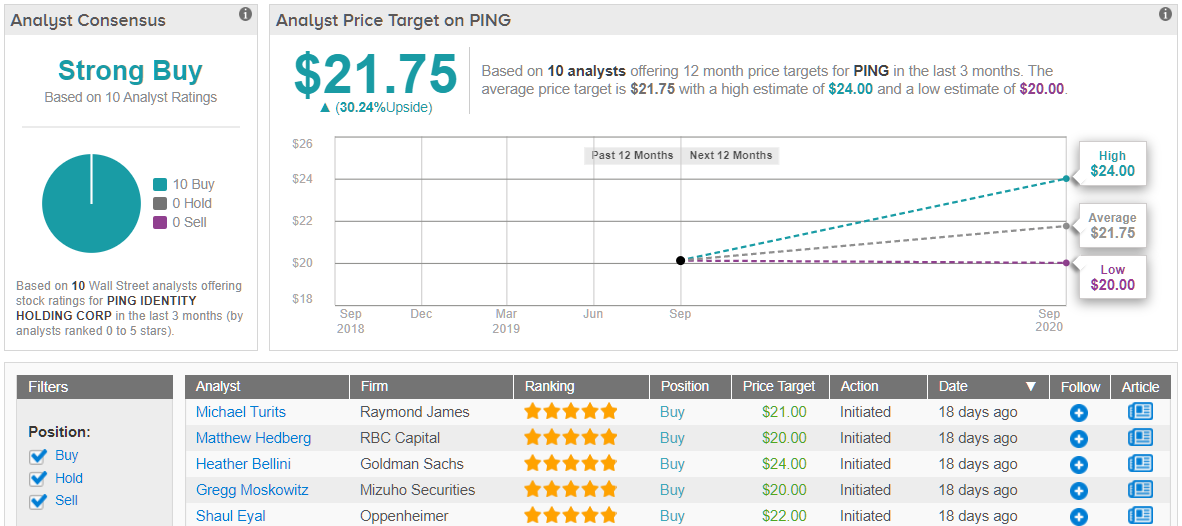

Ping Identity Holding (PING)

Shifting our focus from cannabis to technology, we find Ping. Ping inhabits the security and infrastructure segments of the software sector. The Denver-based company held its IPO just last month, and so does not have a public record of earnings reports to lean on, but its wide variety of products give it a strong position in identity security.

Ping’s products – whether cloud or on-site software based – are designed for a combination of system security and an easy user interface. They are meant to connect users and devices to outside applications through an intelligent platform that treats security in a proactive fashion.

This strong niche position in the security segment hasn’t prevented PING shares from declining sharply since the September IPO. Share price has lost over 15% since then, although the company’s market cap remains above $1.3 billion.

Barclays’ 5-star analyst Saket Kalia sees the fall in share value as a buying opportunity. Finding room for a 23% upside to the stock, he writes: “We initiate on Ping Identity with an Overweight rating and $21 price target given: 1) the $7.5B IAM market is seeing share shift away from tech conglomerates toward security specialists like Ping; 2) Ping casts a wide net with its broad portfolio and flexible deployment, which resonates with enterprises; 3) …we think Ping offers exposure to the important identity and access management (IAM) market at a reasonable valuation and is a good risk-reward at these levels…” (To watch Kalia’s track record, click here)

Kalia is right in-line with the consensus on Ping. Since the IPO, the company has received 10 initiated ratings, all Buys, making the consensus rating of Strong Buy unanimous. Shares are priced at $16.70, and the average target of $21.75 suggests a 29% upside potential. (See PING stock analysis on TipRanks)

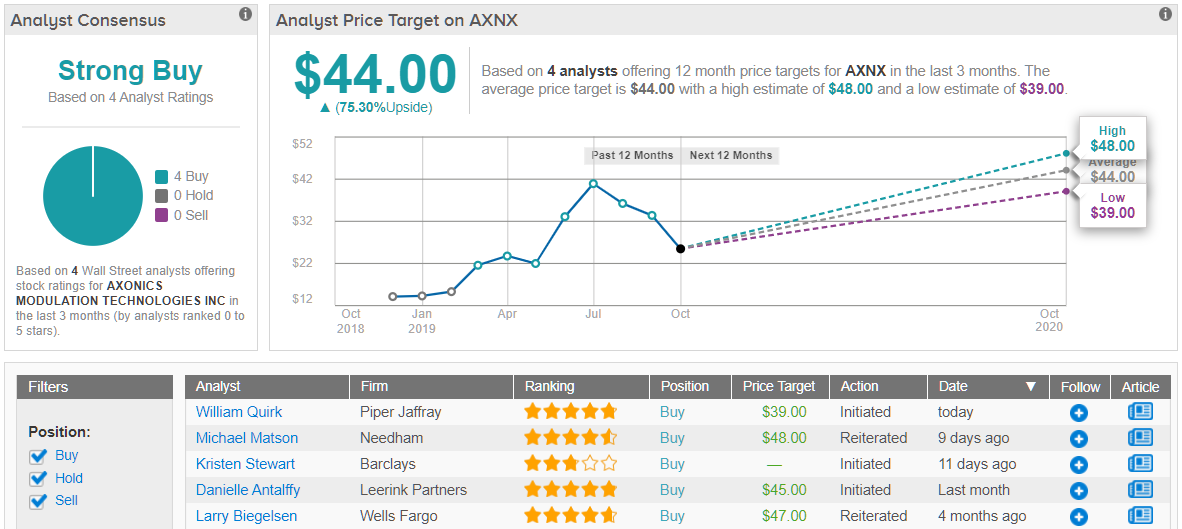

Axonics Modulations Technologie (AXNX)

Switching to the biotech industry, Axonics is another company that has recently gone public. The company inhabits the sacral neuromodulation space, developing non-drug therapies for forms of urinary or fecal incontinence related to weakness in the pelvic floor. The therapy involves implantation of an electrical stimulator for the sacral nerve, the main nerve route from the lower back to the pelvic region.

As populations age, sacral neuromodulation will likely become more popular. It treats a set of common conditions that are related to aging, and has proven effective on symptoms that patients are eager to treat. Axonics products enter this biotech treatment space in direct competition with existing systems and patents developed by competitor Medtronic.

Medtronic, however, has not been able to capitalize on its lead in this market. That company introduced its first approved product back in 1997, and has since launched only one upgrade, back in 2006. This leaves an open space for an aggressive competitor, and Axonics received approval this past September for its own fecal incontinence treatment.

Like the stocks above, AXNX shares have slipped in recent weeks but Barclays sees that as a chance to ‘buy the dip.’ Also like the stocks above, Barclays analyst Kristen Stewart has just initiated coverage of this stock, noting several important points: “We see this as a sales execution story. With a superior product, we believe Axonics can gain share and expand the market—our 40-physician survey supports this view… We believe the pullback has created an opportunity for investors and see the likely FDA approval for urinary indications as a positive catalyst.”

She uses that to support her Buy rating and $43 price target. She also adds, “We believe AXNS has the opportunity to penetrate the $650 million sacral neuromodulation market following FDA approval of its r-SNM system, which we anticipate to occur in 2H19.” Her target implies an impressive upside for the stock, of 77%. (To watch Stewart’s track record, click here)

Overall, the consensus on AXNX is a Strong Buy, based on 3 Buy ratings set in the last month. The stock has an average price target of $46.50, suggesting an upside of 91% from the current share price of $24.27. (See Axonics stock analysis on TipRanks)