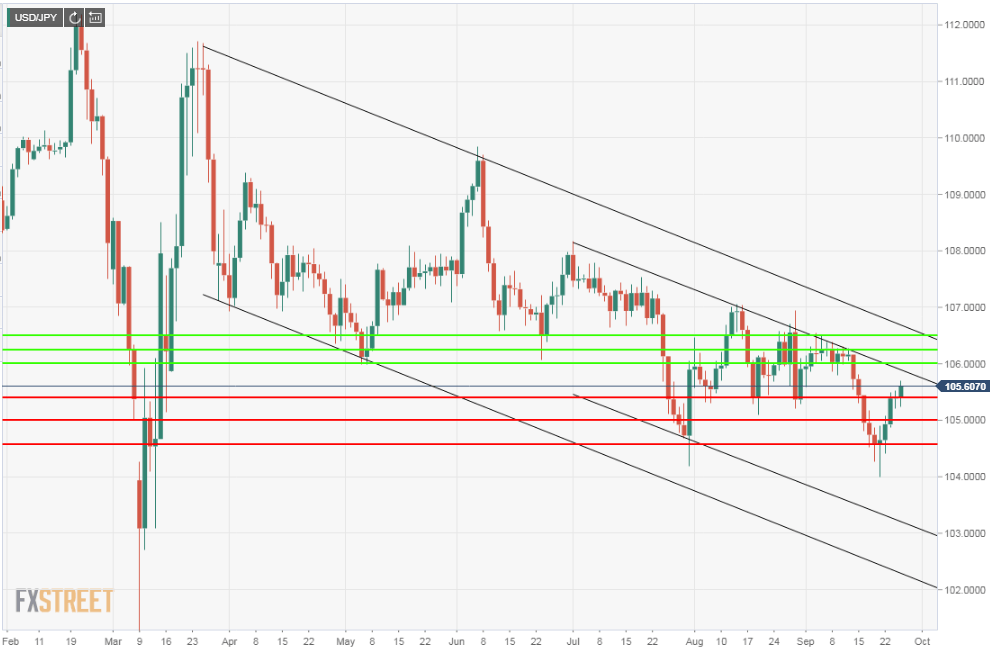

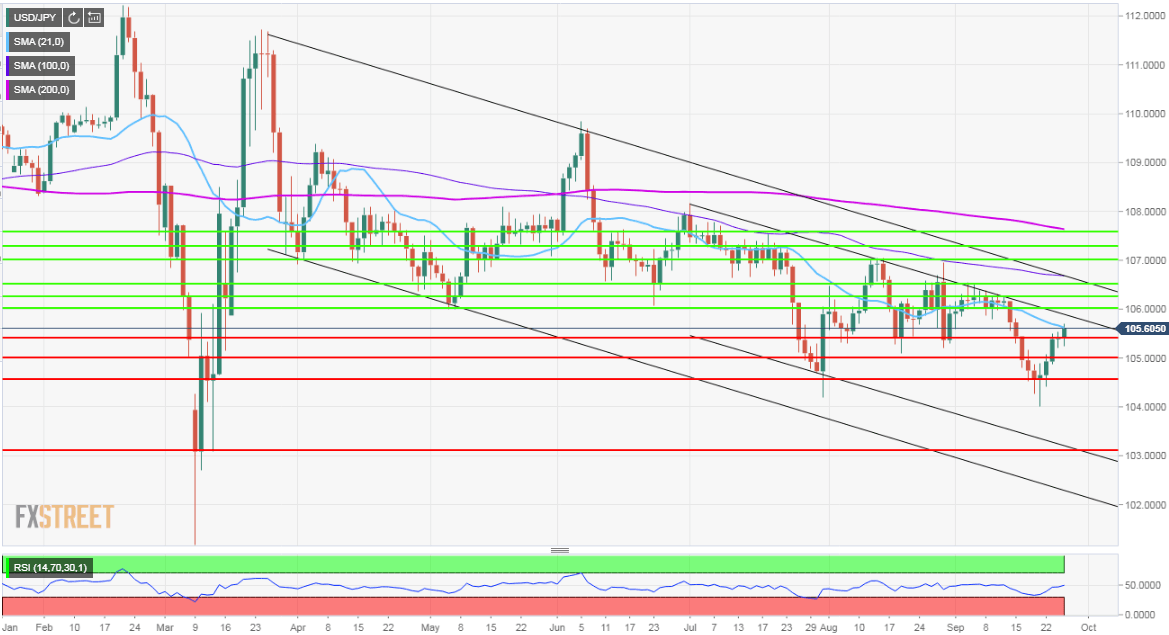

- Descending post-crisis channel from March remains intact.

- Safe haven trade on rising COVID-19 cases aided the dollar this week.

- USD/JPY rise is limited to non-fundamental factors.

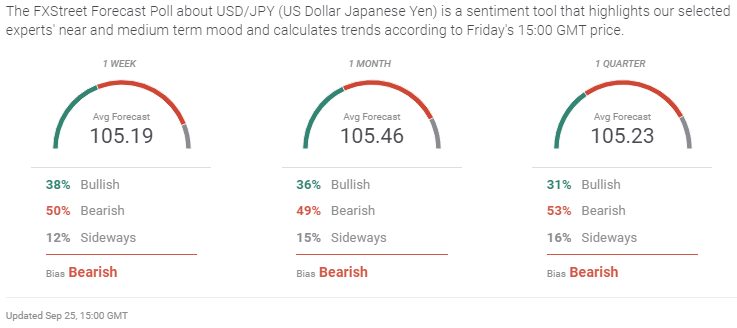

- FXStreet Forecast Poll denotes continuing pressure on USD/JPY.

The gain in the USD/JPY this week was modest, it remained within the narrow down-channel from July and the wider trend from March but the dollar revival shows that the twin specters of the pandemic and economic collapse are never far from traders’ minds.

Though the Japanese yen is often considered a safety currency in its own right the circumstances that foster the response tend to be localized. If China had a resurgence of the virus the yen would respond forcefully. Global, European and American concerns focus on the dollar, the yen partakes but is not the main recipient of flows, with its safety status limiting the dollar’s gain to less than that of other pairs.

Japan’s economy remains stuck in slow growth with little statistical indication of change.

The new Prime Minister Yoshihide Suga has promised to continue former PM Abe’s economic restoration programs of structural reform and deregulation, but their most notable success was the sharp devaluation of the yen in 2012 and 2014.

The current USD/JPY level of 105.60 is well above the first effort which raised the pair from 77 in September 2012 to just under 104 by May 2013. It is not clear that the Bank of Japan or the government would be able to lower the yen from its current rate without the very unlikely cooperation of other central banks.

The USD/JPY reversed at the 104.60 support line in late July and the relatively sharp pullback in the two day’s following Monday’s brief plunge to 104 reinforced the change in direction. Technically the near channel top at 106 coincides with resistance at the same level and is backstopped by another weak line at 106.25.

USD/JPY outlook

The USD/JPY momentum is higher after the sharp reversal this week but it is unlikely to penetrate as far as 107.00 unless there is a more concerted general move to the dollar.

The overall trend contained in the six-month-old channel remains lower even though the economic logic for that direction is weak.

Given the countering tendencies in the pair sideways movement between 105 and 106.50 is the most likely prognosis for the week ahead. A break of 106 and particularly 106.50 would possibly propel the USD/JPY to the two-month high of 107 if the upper border of the descending channel were insufficient to block progress.

Japan and US statistics summary September 21-September 25

Japan had no release of importance this week.

The Jibun Bank Manufacturing PMI for September was 47.3 as expected, 0.1 higher from August. This index has not been above the 50 expansion line since April 2019.

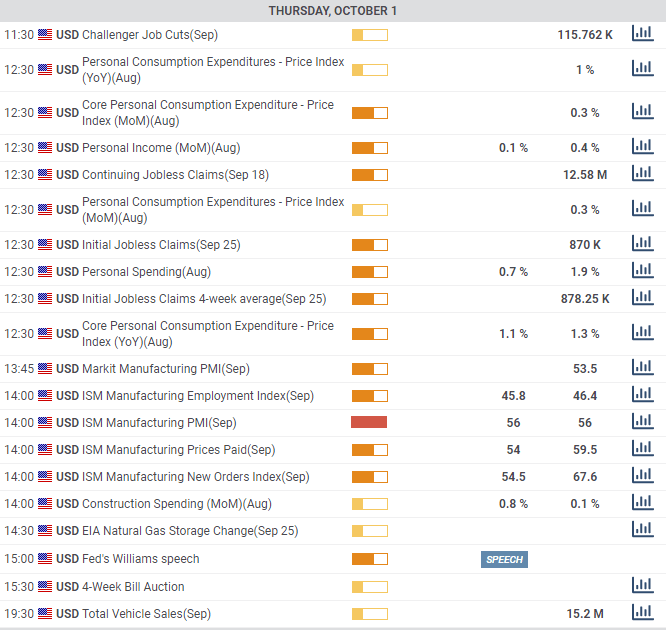

In the US, Fed Chairman Powell and Treasury Secretary Mnuchin testified in Congress three times, calling for continued government support for the economy and a new stimulus bill. It is unclear whether the Democrats and Republicans, in the grip of a presidential campaign, will be able to bring themselves to compromise.

August durable goods order reflected the fading economic support coming in at 0.4% on a 1.5% forecast, though the July number was revised to 11.7% from 11.2%. Non-defense capital goods, the business investment proxy surprised at 1.8%, more than tripling its 0.5% estimate and its July score was revised to 2.5% from 1.9%.

Markit’s preliminary September PMIs were as advertised, 53.5 in manufacturing on a 53.2 forecast and 53.1 in August. The service sector registered 54.6, under its 54.7 prediction and August’s 55.

Jobless claims disappointed with 870,000 filings in the latest week, over the 843,000 prediction and 866,000 in the previous week.

The layoff of nearly one million workers each week is the main negative note for the US economy, showing that some areas of the economy continue to contract.

Japan statistics September 21-September 25

US statistics September 21-September 25

Japan and US statistics summary September 28-October 2

Japan has a relatively crowded week for economic information but only the September releases for CPI and consumer confidence and the August details on retail trade (sales), industrial production and the Tankan Report for the third quarter have potential to encourage movement.

The Coincident Index for July at 76.2 and the Leading Economic Index at 86.9 are expected to be unchanged.

Tokyo CPI is forecast to rise to 0.4% on the year in September from 0.3% and the core rate to gain 0.2% from -0.1%.

August’s retail trade numbers are projected to rise 3.2% after July’s unexpected 3.3% decline. Industrial production is expected to climb 1.5% following July’s 8.7% increase. These are two of the most important figures for the week and any unexpected weakness or strength could lower or support the yen.

The Tankan report on the outlook for large manufacturing and service firms in the third quarter will give an idea on how the established corporate base in Japan views the immediate future and the Capex Index lists business investment. Japan’s economy is still dominated by large export-oriented firms and their health is the basic factor in the economy. Better readings here will support yen.

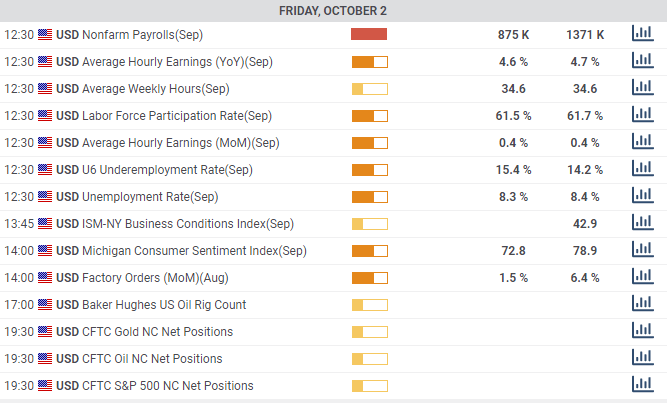

In the US the major news comes from the labor market with the September non-farm payrolls and unemployment data on Friday. Payrolls are expected to drop to 875,000 from 1.371 million in August and the unemployment rate to be largely unchanged at 8.3% from 8.4%.

The recovery of the job market is the main focus for the US economy and the translation is straight forward, better statistics support the dollar and equities. Credit markets are less impacted with the Fed long-term rate hold.

Initial jobless claims are an important secondary data point as the continuing high level of filings undermine confidence in the recovery and tilt the NFP risk lower.

The presidential debate between Donald Trump and Joe Biden on Tuesday, September 29 is not strictly an economic event but any unexpected development or cancellation would roil markets though the specific dollar direction would depend on the circumstances.

Other notable statistics will be the Conference Board Consumer Confidence figures for September, the final revision of second-quarter GDP, Personal Consumption Expenditures and prices for August, ISM manufacturing figures for September and the revision for September's Michigan Consumer Sentiment.

None of these statistics are normally sufficient to provoke markets but the September ISM and the two consumer reading have the most potential.

Japan statistics September 28-October 2

US statistics September 28-October 2

USD/JPY technical outlook

The Relative Strength Index rests at neutral after the close to reciprocal movement of the last two weeks and it is a good representation of the markets' long-term uncertainty for USD/JPY. The 21-day moving average at 105.62 was at market on Friday afternoon with the same logic as the RSI. The 100-day average at 106.68 coincides with the upper border of the wider descending channel and the 200-day average at 107.64 reinforces the 107.60 resistance line.

The multiple resistance lines above the market suggest limited potential for a sustained move higher. Weaker and sparse support and the double descending channel suggest that the risk is downside.

Resistance: 106.00; 106.25; 106.50; 107.00; 107.30; 107.60

Support: 105.40; 105.00; 104.60; 103.25

USD/JPY Forecast Poll

The sentiment may be uniformly bearish across all three timeframes in the FXStreet Forecast Poll but there is no evident trend. The one-week and one-quarter forecasts are within points of each other and the one-month estimate is 27 points above the earlier and 23 points above the latter. Technical indicators suggest weakness in the USD/JPY but they also hint that the six-month downtrend is nearing exhaustion.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

EUR/USD holds above 1.0650 after US data

EUR/USD retreats from session highs but manages to hold above 1.0650 in the early American session. Upbeat macroeconomic data releases from the US helps the US Dollar find a foothold and limits the pair's upside.

GBP/USD retreats toward 1.2450 on modest USD rebound

GBP/USD edges lower in the second half of the day and trades at around 1.2450. Better-than-expected Jobless Claims and Philadelphia Fed Manufacturing Index data from the US provides a support to the USD and forces the pair to stay on the back foot.

Gold clings to strong daily gains above $2,380

Gold trades in positive territory above $2,380 on Thursday. Although the benchmark 10-year US Treasury bond yield holds steady following upbeat US data, XAU/USD continues to stretch higher on growing fears over a deepening conflict in the Middle East.

Ripple faces significant correction as former SEC litigator says lawsuit could make it to Supreme Court

Ripple (XRP) price hovers below the key $0.50 level on Thursday after failing at another attempt to break and close above the resistance for the fourth day in a row.

Have we seen the extent of the Fed rate repricing?

Markets have been mostly consolidating recent moves into Thursday. We’ve seen some profit taking on Dollar longs and renewed demand for US equities into the dip. Whether or not this holds up is a completely different story.