The relentless selling pressure in the Gold Miners Index (GDX) has finally come to an end in April, with the index turning up sharply and erasing its year-to-date decline. This incredible recovery has occurred despite the fact that gold (GLD) remains in negative territory for the year, suggesting that we could see a large rally ahead for miners if gold can regain its momentum. While many investors are likely nervous about jumping in miners here after a 3-week rally, it’s important to note that many miners are still very reasonably valued, and there are a select few that look like solid buy-the-dip candidates. We’ll take a look at three of these names below, highlighting what makes them special amongst their peers:

(Source: TC2000.com)

The safest way to gain leverage to the price of gold is the GDX, but with several names unable to post positive returns over a 2-year, 5-year, and 10-year basis, many laggards often drag down the index and weigh on its performance. This means that for those willing to do their research or select the top-tier names, one can gain leverage on the index without having ones’ performance partially tied to the serial underperformers within the group. In this update, we’ll look at three stand-out names with exceptional business models, pay competitive dividend yields, and have mines in predominantly safe jurisdictions. These three companies are Newmont (NEM), SSR Mining (SSRM), and Alamos Gold (AGI), with two being intermediate producers (400,000 plus ounces of production per annum) and one being the largest producer in the world. Let’s take a closer look at each name below:

Beginning with Newmont, the company just came off of a strong year and also posted a very impressive mineral reserve update in FY2020. Despite COVID-19 weighing on operations and making it more difficult to drill to add reserves, Newmont reported FY2020 free cash flow of $3.6BB and an industry-leading reserve base of ~95MM ounces. This was down only marginally year-over-year, even though NEM maintained its conservative metals price assumption of $1,200/oz for calculating reserves. This means that if NEM were to move its metals price assumption to $1,400/oz, which would still be very conservative relative to spot prices, its reserve base would increase to closer to 110MM ounces. With a production profile of 6MM ounces per annum, this translates to 18 years of mine life at $1,400/oz, and a ~16-year mine life at $1,200/oz.

(Source: YCharts.com, Author’s Chart)

Some investors argue that it’s wrong to value gold miners on a price-to-earnings basis, given that there’s significant volatility in the gold price and a company’s ultimate mine life is finite. This is true, of course, and does suggest that investors should discount the fair earnings multiple used for gold miners. However, with visibility into 2036 in terms of maintaining similar production levels, I don’t see any issue with valuing NEM at 20x earnings. Based on FY2021 annual EPS estimates of $3.97, NEM’s fair value far exceeds its current share price, even after the recent rally. This is because fair value is sitting at $79.40, more than 20% above current levels. Besides, investors are getting an annual dividend of between $2.20 to $2.50 based on a $1,600/oz to $1,800/oz gold price, translating to a nearly 3.80% yield at the high end of this range. So, with a 20% discount to fair value and a very competitive yield, I would expect any dips below $60.00 on NEM to provide buying opportunities.

(Source: Company Filings, Author’s Chart)

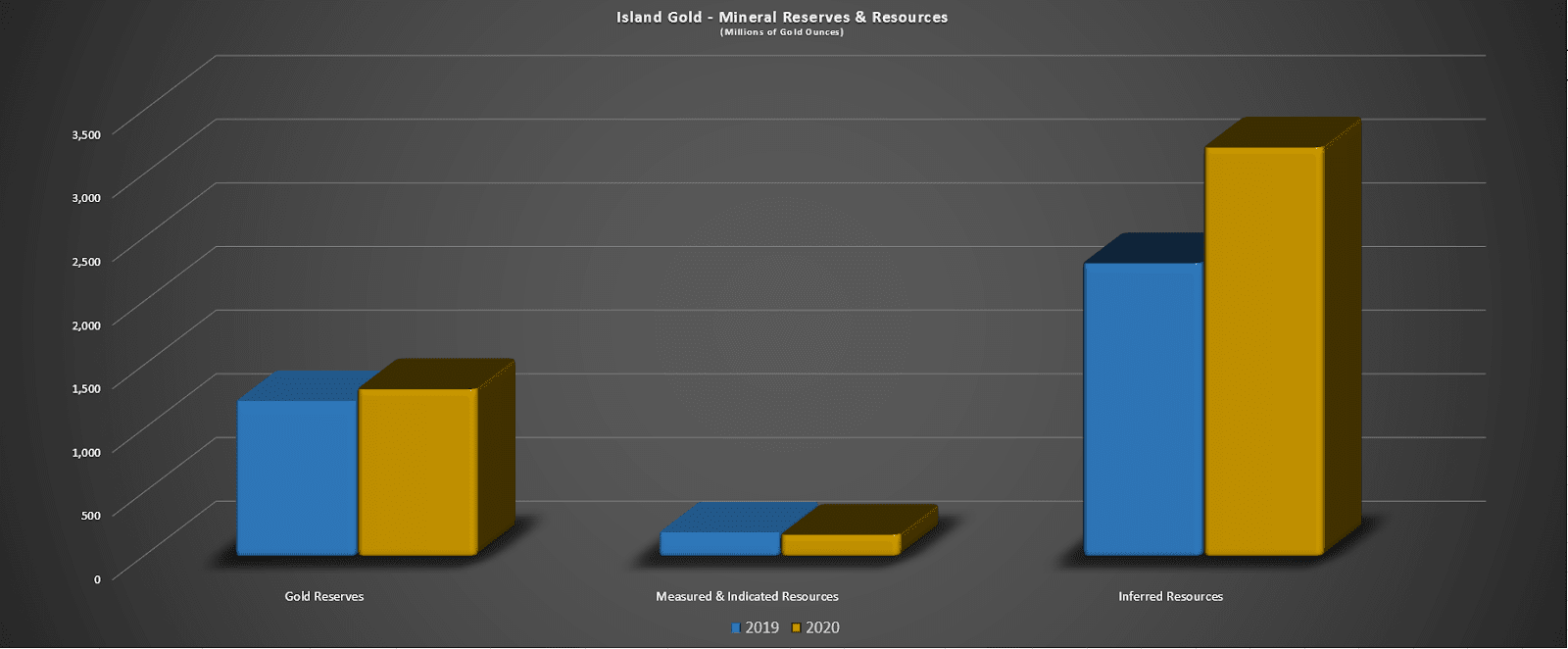

The next name on the list is Alamos Gold, an intermediate gold producer with operations in Canada and Mexico. The company recently announced its mineral reserve update for FY2020 and was one of only nine companies to report an increase in mineral reserves despite maintaining its very conservative gold price assumption of $1,250/oz. However, the biggest news was from the company’s Island Gold Mine in Ontario. Not only did Alamos increase its reserve base net of ~140,000 ounces of mining depletion to well above 1 million ounces, but it saw a massive boost in its inferred resource base at the mine (separate from reserves). Assuming a conservative conversion rate of resources to reserves of 70%, the Island Gold Mine could have an 18+ year mine life, which would support its growth plans to ~236,000 ounces per year by FY2025 (from 140,000 ounces currently). With this mine set to enjoy all-in sustaining costs of below $550/oz, Alamos is set to see significant margin expansion starting in 2024, looking out until the late 2030s.

(Source: YCharts.com, Author’s Chart)

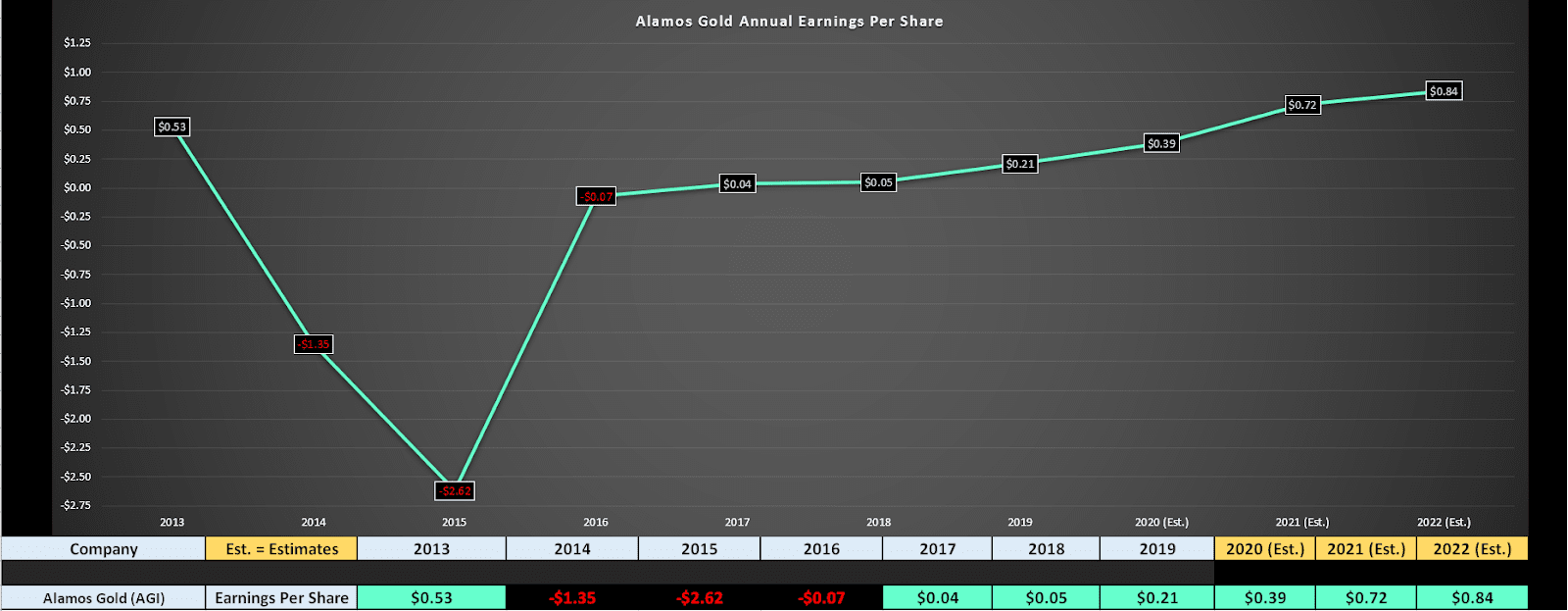

If we look at the company’s earnings trend, Alamos is set to see a new all-time high in annual EPS in FY2021, with annual EPS estimates sitting at $0.72. If we look ahead to FY2022, annual EPS estimates are at $0.84, and they should hit $1.00 by FY2024 even if the gold price remains below $1,900/oz. So, at a share price of $8.70 with more than $1.00 in cash, Alamos is trading at less than 8x FY2024 annual EPS and barely 10x FY2021 annual EPS estimates. If Alamos was a low-growth without organic growth potential, this valuation might make some sense. However, Alamos is planning to grow production from 500,000 ounces per year in FY2021 to 750,000 ounces in FY2025, and this justifies an earnings multiple of at least 15 when we factor in Alamos’ industry-leading margins by FY2023.

Assuming Alamos reports $1.00 in annual EPS in FY2024, this translates to a fair value of $15.00, or more than 75% upside from current levels. It’s important to note that this price target is based on a $1,800/oz gold price, and upside in the gold price could easily push FY2022, FY2023, and FY2024 estimates to significantly higher levels, increasing this price target materially. Therefore, if we see AGI dip below $8.00, I would view this as a low-risk buying opportunity.

(Source: YCharts.com, Author’s Chart)

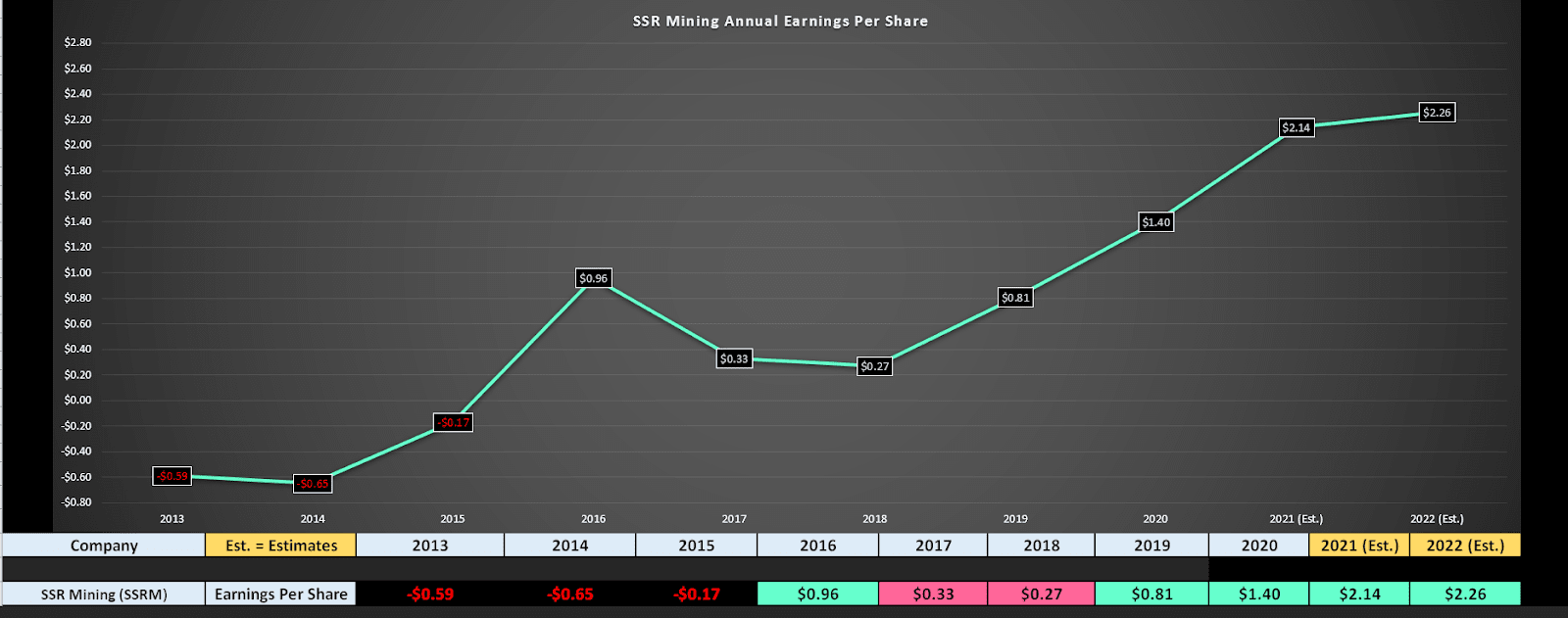

The final name on the list is SSR Mining, a company that has been unfairly punished after its merger with a gold producer operating out of Turkey, Alacer Gold. While Turkey is not the most attractive jurisdiction, it’s important to note that more than 50% of SSRM’s production comes from outside Turkey, with mines in Nevada, Canada, and Argentina. Besides, the recent pullback looks like it’s more than priced in the jurisdictional risk after the merger, with SSRM trading at less than 12x trailing earnings of $1.40 and less than 8x FY2021 annual EPS estimates of $2.14. So, for investors willing to step out on the risk curve a little, pullbacks below $15.80 should provide low-risk buying opportunities. It’s important to note that SSRM is the highest risk name on the list, but it also offers material upside, with a conservative fair value this year of ~$21.00 based on a earnings multiple of just 10.

The GDX has had a nice run the past few days, and some weakness would not be surprising to shake out some weak hands. However, AGI, NEM, and SSRM look like solid buy-the-dip candidates if a pullback does materialize, and I see no reason to cash in profits on these names just yet. Assuming gold can get back above $1,875/oz, these stocks all have at least 30% upside over the next 12 months, and the bonus is that investors are getting paid to wait with a yield ranging from 1.20% to 3.50% yield across the three names.

Disclosure: I am long GLD, NEM, AGI

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

NEM shares were unchanged in after-hours trading Thursday. Year-to-date, NEM has gained 10.77%, versus a 10.63% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles. More...

More Resources for the Stocks in this Article

| Ticker | POWR Rating | Industry Rank | Rank in Industry |

| NEM | Get Rating | Get Rating | Get Rating |

| SSRM | Get Rating | Get Rating | Get Rating |

| AGI | Get Rating | Get Rating | Get Rating |

| GLD | Get Rating | Get Rating | Get Rating |

| GDX | Get Rating | Get Rating | Get Rating |