Weekly Ag Markets Update - Monday, April 26

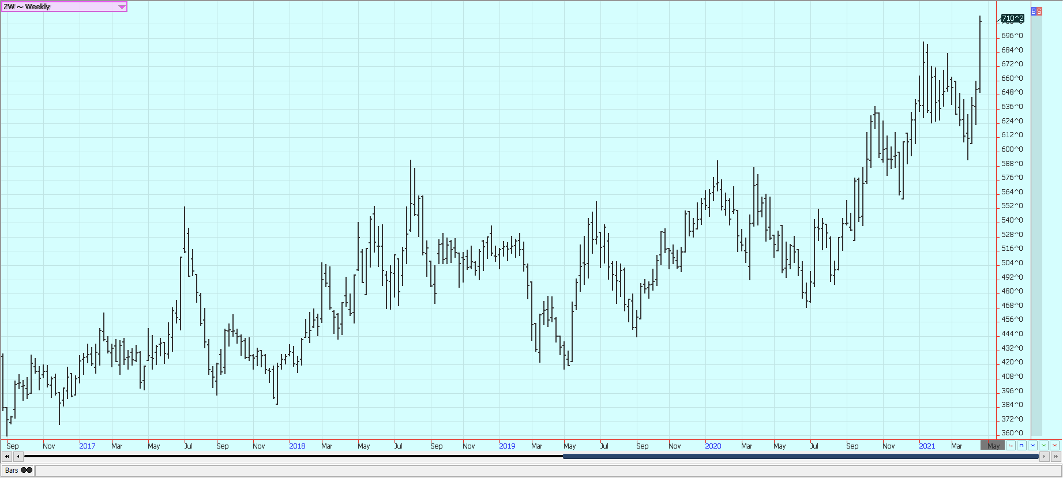

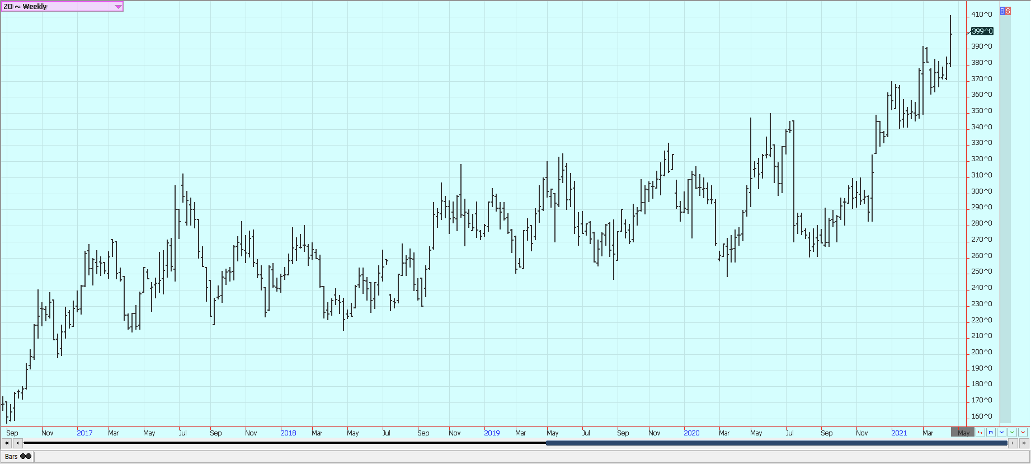

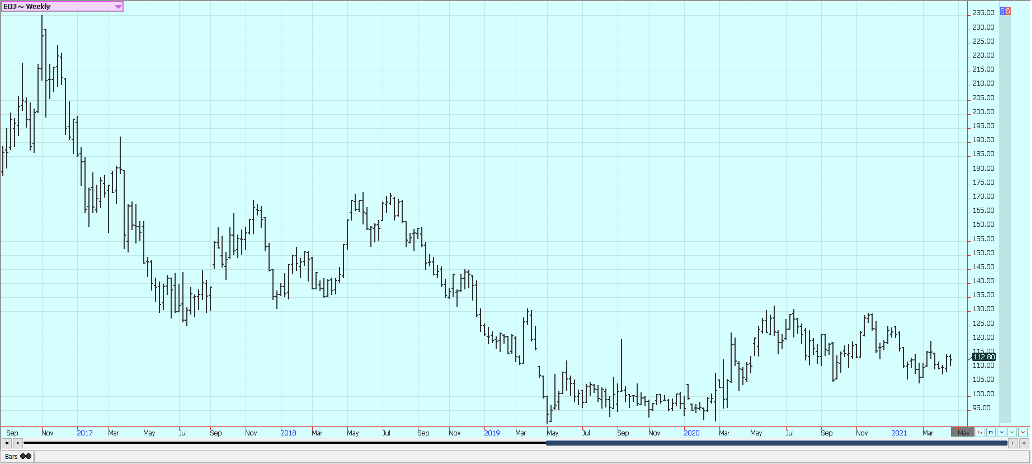

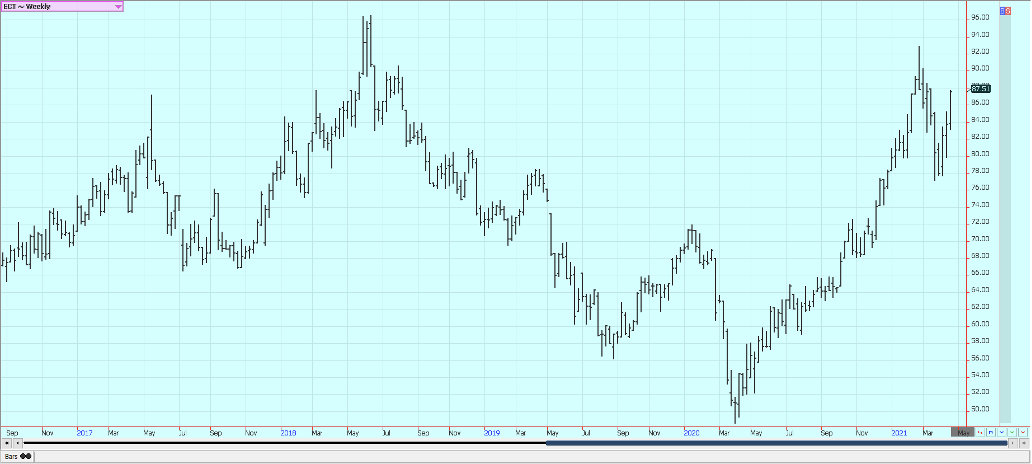

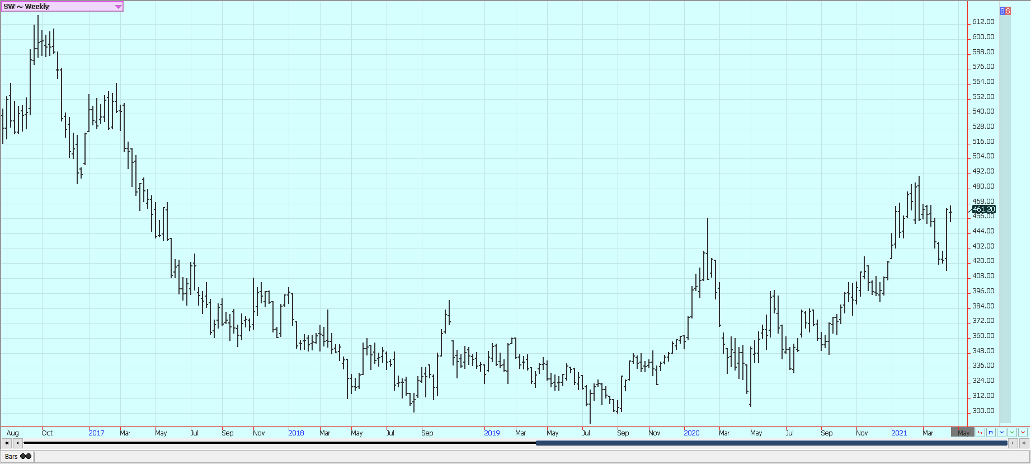

Wheat: Wheat markets were sharply higher on Friday and for the week as Wheat remains a weather market. The weather remains too dry in the northern Great Plains and in the Canadian Prairies and farmers have planted into dry soils. It has been very cold and some Winterkill was possible in the central and southern Great Plains as well as the Midwest. The most damage from the freezing temperatures was expected to be in Oklahoma. There will be some precipitation with the colder air which should be mostly light but beneficial for the short term. Demand remains disappointing but the production might not be there for better demand in the coming year. Corn prices are high so demand for feed wheat could increase. The chart trends are up on the daily charts and on the weekly charts.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed sharply higher last week on what appeared to be additional speculative buying based on ideas of strong demand and long term weather outlooks for warm and dry weather west of the Mississippi River. Futures were mixed on Friday, with nearby months higher and new crop months a little lower. Oats closed lower on Friday but higher for the week. It was very cold last week in the US and some recently planted Corn could have been hurt or at least be very slow to emerge. Temperatures will be warmer this week but there will be precipitation to keep farmers from the fields. There are also concerns about the production potential for the Safrinha crop in Brazil as growing areas have been warm and dry and look to stay that way longer term. Oats were higher. There is talk of new Chinese interest in buying US Corn. Chinese demand had been strong until recently and it looks like they need the Corn. Prices inside China for Corn remain extremely high. It is drier in central and parts of northern Brazil, and farmers have finally harvested the Soybeans area and planted the Winter Corn. The Winter Corn crop progress is well behind normal and it has been dry in major growing areas. Demand for US Corn has been coming at a stronger pace than estimated by USDA and it looks like the US ending stocks can be significantly less than current projections by the end of the year.

Weekly Corn Futures

Weekly Oats Futures

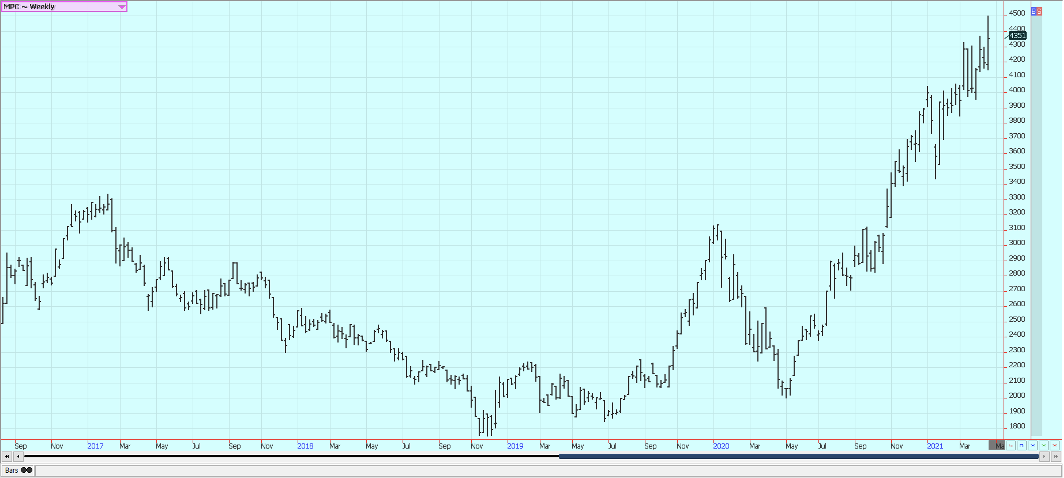

Soybeans and Soybean Meal: Soybeans and the products were sharply higher. There is still crush demand and export demand even though the demand is less now than before and the market thinks the US is going to run out of Soybeans unless demand can be rationed with high prices. The US does not have a lot of Soybeans in the country anymore as most producers have already sold. Buyers are scrambling for what is left. Brazil is rapidly exporting Soybeans. The Brazil harvest had been delayed due to late planting dates early due to dry weather and now too much rain that has caused harvest delays and some quality problems in the north as well. Harvest activities are done now. China has been buying for next year here but now is buying mostly in South America.US internal demand has been strong. Soybean Meal is under pressure due to the big buying seen in Soybean Oil although both were higher yesterday. Production of DDG can increase in the near future as ethanol demand improves and more people start driving again.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

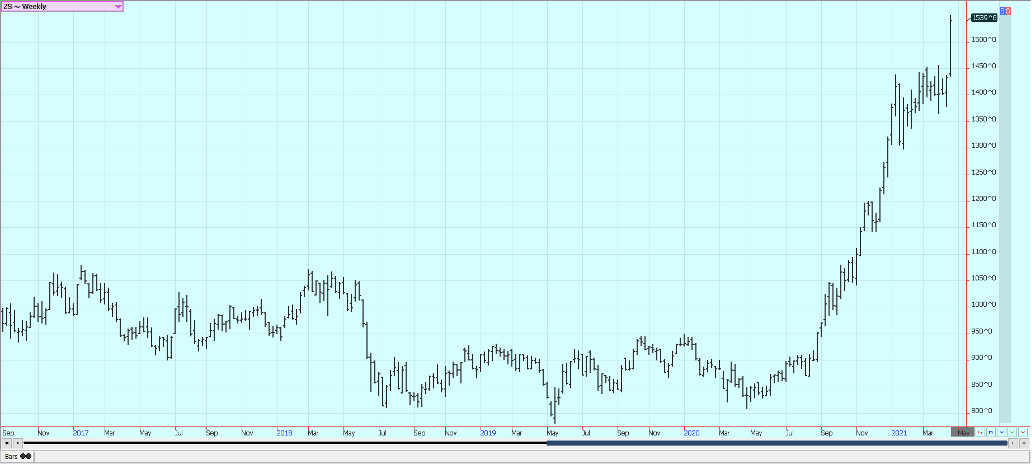

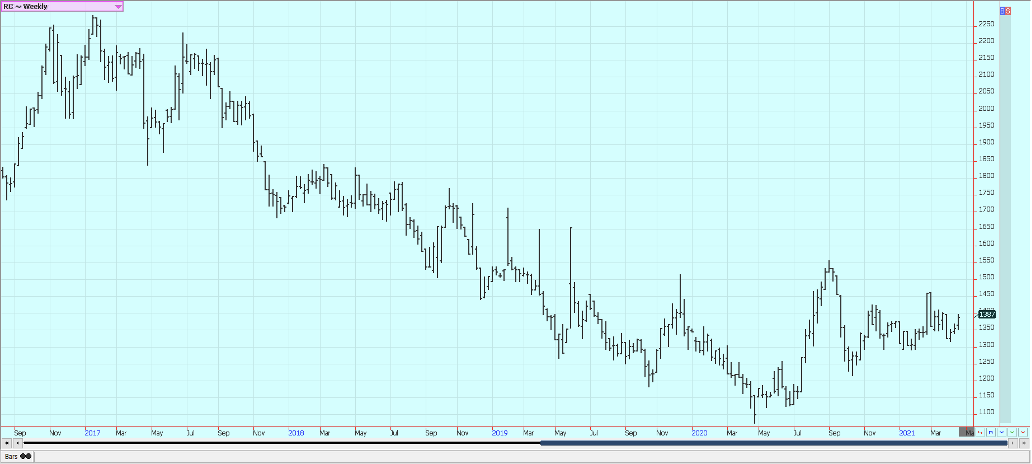

Rice: Rice was sharply higher last week on what appeared to be big fund buying on Thursday. There did not seem to be a real good reason for the rally, but the weekly export sales report showed good sales. Demand has been solid for exports but less for the mills and this remains the feature of the trade. The export demand has been primarily for paddy Rice and not for milled Rice. The cash market has not felt any increased demand lately and mill operations are reported to be on the slow side. Texas is about out of Rice, but there is Rice available in the other states, especially Arkansas. Asian and Mercosur markets were steady to lower last week. New crop months were a little lower. New crop Rice is getting planted in Texas and planting is more than three-quarters done in Louisiana. Mississippi and Arkansas are starting planting. It will be cold for the next few nights but the Rice should not be affected as it is still not really in the ground yet.

Weekly Chicago Rice Futures

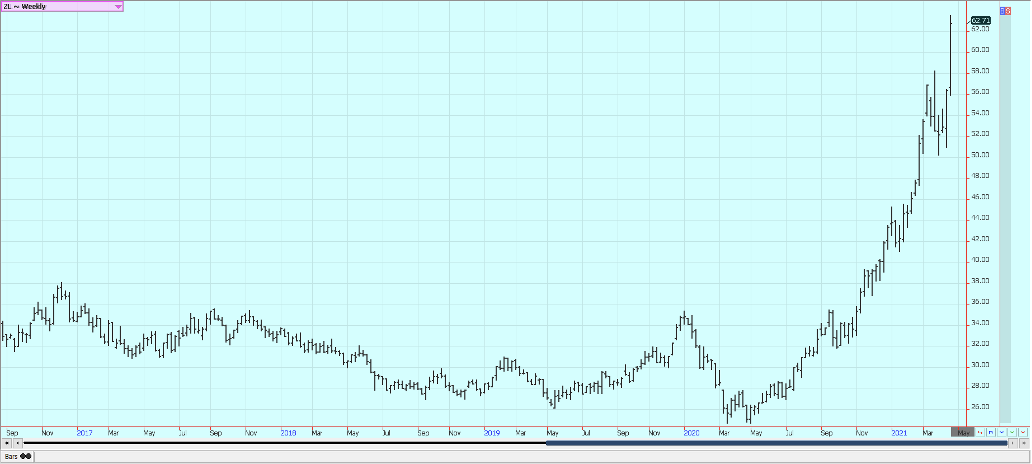

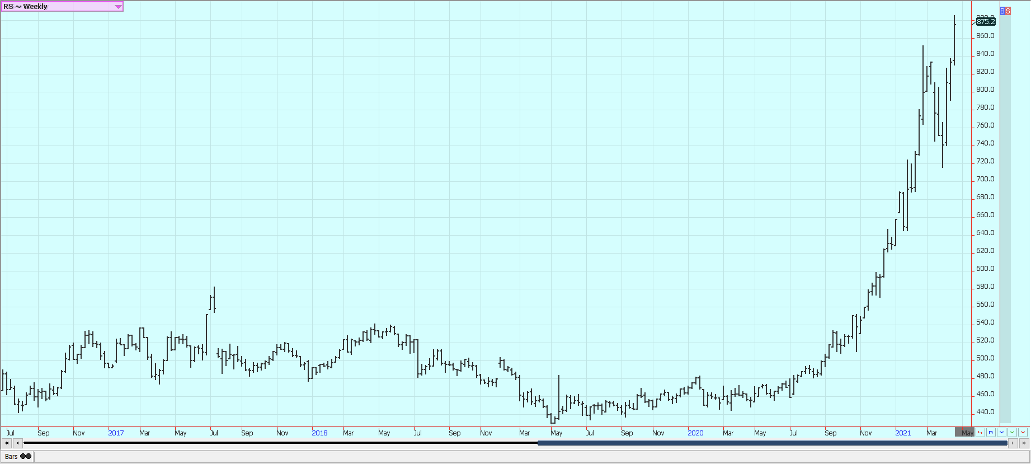

Palm Oil and Vegetable Oils: Palm Oil was lower on Friday but higher for the week on good demand and price action in the other competing markets. The private sources showed that export demand is running well ahead of last month so far this month. Ideas of tight supplies are still around but MPOB did show higher than expected ending stocks in its March data released last week. An analyst said on Friday that supplies available to the market would increase over the next several months. The production of Palm Oil is down in both Malaysia and Indonesia. Canola was higher on ideas of tight supplies combined with a drought in the Canadian Prairies. Canada has bought a couple of cargoes of Rapeseed from Ukraine and might buy more due to price spreads between the two producing countries. Worries about South American production are supporting both markets as is cold and dry weather in the Prairies. Demand is thought to be great with crush margins favoring a lot of production of vegetable oils to feed the demand. The demand for bio fuels is about to increase and is one reason to see much stronger Soybean Oil and Canola prices.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

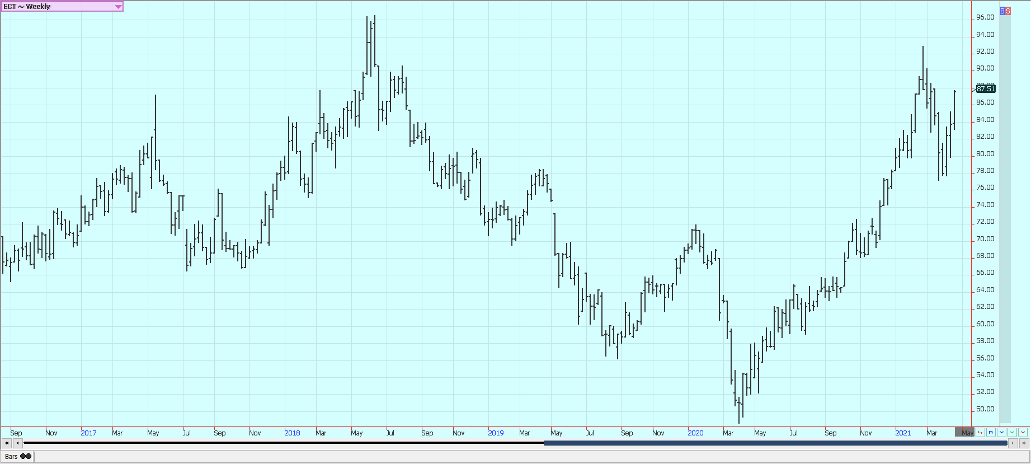

Cotton: Futures were higher on Friday and for the week as cold weather is threatening newly planted Cotton in Texas, but nearby months were a little lower on the weaker demand seen in the export sales report. Chart patterns still suggest that a bull flag is trying to form. Temperatures are likely to dip below freezing. The demand for US Cotton in the export market has been strong even with the Coronavirus causing disruptions at the retail level around the world. The US stock market has been generally firm to help support ideas of a better economy here and potentially increased demand for Cotton products. It is dry in western and southern Texas and the planting of Cotton is being delayed. Some showers are expected in western areas in the next couple of days to help there, but it is still dry overall.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher in range trading. Futures are still trying to force a big low at this time. The demand for FCOJ is said to be weaker. The weather has turned warmer so less flu is around and the increased vaccination pace means that the coronavirus is less. Moderate temperatures are expected for Florida this week. The weather in Florida is good with a few showers or dry weather to promote good tree health and fruit formation. The hurricane season is coming and a big storm could threaten trees and fruit. That is still a couple of months away. It is dry in Brazil and crop conditions are called good even with drier than normal soils. Stress to trees could return if the dry weather continues as is in the forecast. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. It is dry in northern and western Mexican growing areas.

Weekly FCOJ Futures

Coffee: New York and London closed higher on Friday and higher for the week as the fears of dry weather impacting the Brazil production continued. The main feature to the market is the weather in Brazil and the production prospects in the country. Some cooperatives and the export association are calling for a significant reduction in production with a 30% loss in production potential mentioned. It was dry at flowering time and has been dry again recently. It is also the off-year in the two-year production cycle. Production conditions elsewhere in Latin America are mixed with good conditions reported in northern South America and improved conditions reported in Central America after devastating floods early in the growing cycle. Conditions are reported to be generally good in Asia and Africa.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York closed a little higher and London closed a little lower last week as fears of dry Brazilian weather continued. Ideas of stronger Ethanol demand helped support Sugar prices last week as the competition is back for crushing and refining use. Current Sugar demand is called average. Dry conditions were reported in Brazil. The primary growing region has been dry overall but recent rains that have fallen have been very timely. Production has been hurt due to dry weather earlier in the year. Traders are worried about a delayed Brazil harvest and lack of space at Brazil ports for Sugar shipments due to the high Soybeans shipments and delayed nature of the harvest of the Soybeans. India is exporting Sugar and is reported to have a big cane crop this year. The harvest there is almost over so offers are being reduced. Thailand is expecting improved production after drought-induced yield losses last year. Exports are expected by USDA to be higher in the coming year. The EU had big production problems last year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed higher in range trading. The grind data overall showed improved demand when it was released last week. The main crop harvest is over in West Africa and the mid crop harvest is active. Ports in West Africa have been filled with Cocoa. That is changing a bit as the governments of Ivory Coast and Ghana have given up on their fair wage scheme to try to tax exporters and buyers. European demand has been slow as the quarterly grind data showed a 3% decrease from a year ago in grindings. This has been caused by less demand created by the pandemic. Asian demand improved. North American data showed improved demand.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

Disclaimer: A Subsidiary of Price Holdings, Inc. – a Diversified Financial Services Firm. Member NIBA, NFA Past results are not necessarily indicative of future results. Investing in ...

more