Once again, Norway's central bank leads the pack on interest rate hikes, and the clear hawkish central bank bias should help the krone outperform other cyclical G10 currencies. We continue to see EUR/NOK testing 10.00 over the coming months.

Unsplash

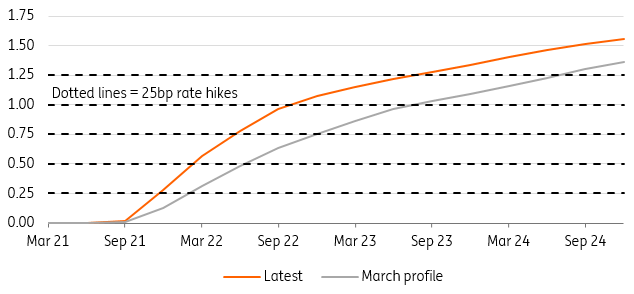

Four hikes by the end of 2022 in Norway

Norway’s central bank has once again cemented itself as a hawkish outlier in the G10 policymaker arena. Norges Bank is now pencilling in its first rate hike in September, and its rate projection indicates that may well be followed by another in December and March of next year. In total there are four hikes in by the end of next year, and another couple by the end of 2024.

In a sense none of this is too surprising. The Norges Bank had already been signalling at least one hike this year, and in effect the latest rate path just adds in one additional hike over what was in the March profile. The bounceback in Norwegian activity, coupled with slightly higher oil prices and a weaker NOK (relative to what the central bank says it would expect given energy price levels), all contributed to the higher rate path.

At this stage, there’s little reason to doubt that these rate hikes will materialise, barring further Covid-19 surprises. But does this tell us much about what other central banks might do? We suspect it doesn’t. Remember back in 2019, the Norges Bank hiked interest rates three times, while the Fed was busy cutting.

Norges Bank interest rate projection: Now vs. March

Source: Norges Bank

NOK: Hawkish NB but the Fed matters more

While the central bank cemented its place as the most hawkish central bank in the G10 FX space, the positive spill over into NOK was rather brief, and the krone gains short-lived this morning. We see the NB’s signal to start its hiking cycle in September as a positive for NOK, but at this point, the external environment driven by the hawkish Fed matters more. Hence, the limited EUR/NOK decline in response to the meeting. Were it not for the Fed yesterday, EUR/NOK would have been below 10.00 today, in our view.

Still, the clear hawkish bias should help NOK outperform other cyclical G10 currencies in the coming months.

As per the Fed review, we think it may be too early to wave a white flag for carry trades going into the summer and with NOK likely to benefit from the highest implied yield in the G10 space by the year-end, the currency should stay supported over the summer, particularly against the euro which looks likely to be used as a go-to funding currency this summer. We continue to see EUR/NOK testing 10.00 in the coming months.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.