- UBS forecasts that Q2 earnings for the S&P 500 (SP500) (NYSEARCA:SPY) should beat consensus estimates by more than 15%.

- "Our top-down earnings model points to Q2 EPS of $51.5+, which would be earnings growth of 80%+ yoy," strategists led by Keith Parker wrote in a note this past week. "Recent revisions for earnings, sales and margins have been positive and broad across sectors and industries, with margin downgrades concentrated in a few industries."

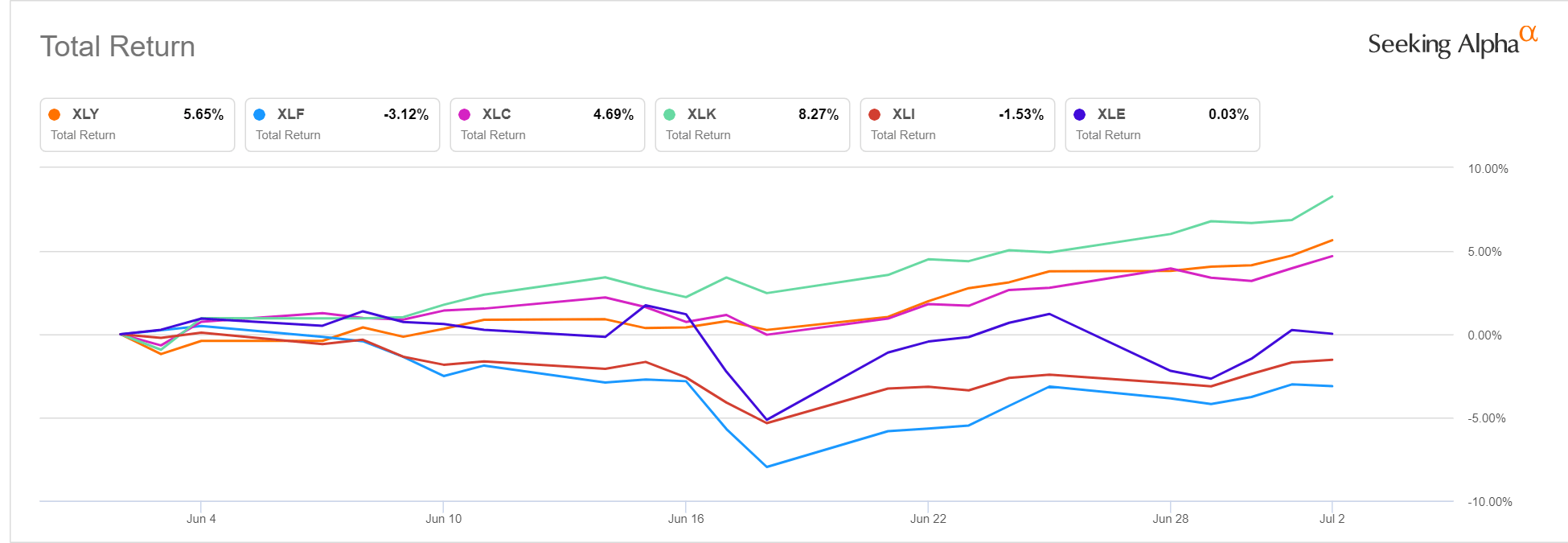

- The team looked at the sectors that have the most upside and, again, cyclicals are high on the list.

- "Comparing Q2 EPS revisions to Q1 beats as well as recent EPS momentum, we see broad-based upgrades, likely led by Cons Discretionary (NYSEARCA:XLY), Financials (NYSEARCA:XLF) and Media & Enter (NYSEARCA:XLC), with solid momentum for Tech (NYSEARCA:XLK) and Industrials (NYSEARCA:XLI)," Parker writes. "Energy (NYSEARCA:XLE) and Materials (NYSEARCA:XLB) earnings momentum remains robust."

- "We see mixed trends for Healthcare Equip & Svcs and Food & Bev - and much less upside for most defensive industries compared to cyclicals."

- Year-to-date, XLY is up nearly 13%, while XLF is up 25%, Communications Services, which comprises most media and entertainment, is nearly 22% higher, while XLK is up 15% and XLI is up nearly 17%.

- Parker also lists the themes to watch during earnings season:

- Margins at peak, but drivers supportive. "Sales acceleration, productivity, price increases and operating leverage point to meaningful new margin highs near-term in our frameworks with continuing support. Cost pressures are concentrated in a few industries in our work. However, margin outlooks will be key for stocks over coming quarters and a major focus of investors amid rising inflation."

- Pricing power. "Consensus expects EBIT margins for strong pricing power stocks to fall 55bp in Q2 on avg, vs. a 50bp jump in Q2 and 120bp surge in Q3 for weak pricing power. Rising input costs is a downside risk for weak pricing power stocks. Indeed, margin revisions have turned in favor of strong pricing power stocks (vs. weak), pointing to relative upside for estimates."

- Payouts vs. capex. "As a % of earnings, S&P 500 dividends+buybacks are 12pp below the 10y average, pointing to a big jump in both payouts ahead. Indeed, buyback announcements have surged, and should continue to rise."

- Check out UBS' list of top stocks with pricing power.