- DexCom (NASDAQ:DXCM) reached an all-time high on Friday after the company’s Q2 2021 results exceeded analyst expectations.

- The maker of continuous glucose monitoring systems attributed the outperformance to the strength in salesforce and direct-to-consumer marketing in the U.S.

- Meanwhile, the international business growth accelerated thanks to the impact of the pandemic in the prior-year quarter.

- While Dexcom recorded its best one-day gain in more than 20 months following a guidance raise for 2021, the analysts at Baird recommended investors to buy the stock despite the strength.

- “End markets seem near fully recovered, DXCM's competitive positioning has improved, investments are paying off,” analysts Jeff D. Johnson and Dane Reinhardt argued as they raised the price target to $520 from $460 to imply a premium of ~14% to pre-earnings close.

- Listing several catalysts in the company’s near and medium-term timeframe, they reiterated the outperform rating with a bullish view on the growth outlook for several years.

- The duo expects the company, as highlighted by the management in the earnings call, to launch its next-gen G7 CGM system in late 2021.

- In addition, they also have an upbeat view on the upcoming commercial rollouts of Automated Insulin Delivery systems with Dexcom’s glucose monitoring systems such as Omnipod 5 from Insulet (NASDAQ:PODD), which according to management, has a “strong pent-up demand.”

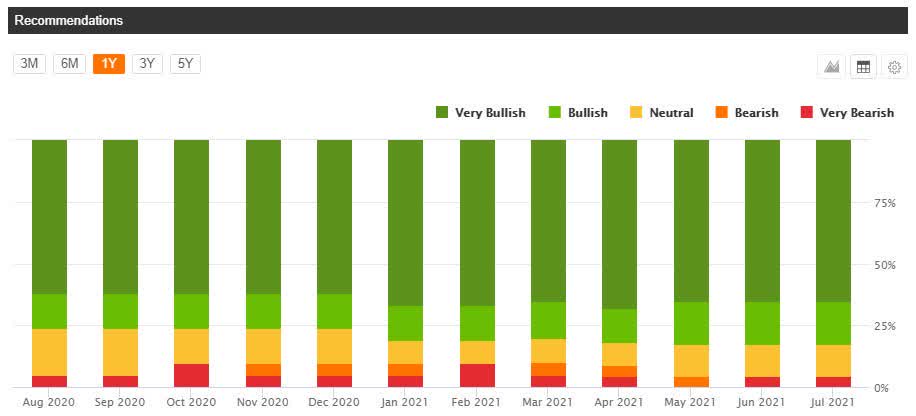

- DexCom has added nearly 20% over the past 12 months, with a concurrent rise in bullish recommendations from Wall Street analysts, as indicated in the graph below.