Independent identity management services provider Okta, Inc. (OKTA) delivered strong second-quarter results with a 59% growth in subscription revenue and a 57% increase in its remaining performance obligation (RPO) to $2.24 billion. However, shares fell 2.6% on the news in the extended trading session on September 1.

Okta reported a quarterly loss of $0.11 per share, much better than analysts’ estimated loss of $0.35 per share. In the year-ago period, Okta posted earnings of $0.07 per share.

To add to that, total revenue grew 57% year-over-year to $315.50 million and surpassed the Street’s estimate of $296.23 million. (See Okta stock charts on TipRanks)

On May 3, Okta completed the acquisition of Auth0, which contributed around $38 million towards total revenue in the second quarter.

Commenting on the results, Todd McKinnon, CEO and co-founder of Okta, said, “Execution remained sharp with strong demand for Okta’s workforce and customer identity solutions, as well as Auth0’s developer-centric identity solutions.”

McKinnon added, “As organizations advance on their journey of improving their customers’ digital experience, adopting zero-trust security environments, and deploying more cloud applications, they continue to turn to Okta to deliver an unmatched array of modern identity solutions to meet these challenges.”

The company provided Q3 and full-year fiscal 2022 guidance to include the expected contribution from its Auth0 acquisition.

In Q3, Okta forecasts revenue to fall in the range of $325 – $327 million compared to the consensus estimate of $322.93 million. The third-quarter loss is expected to range between $0.25 – $0.24 per share versus the consensus-estimated loss of $0.34 per share.

Additionally, for the full fiscal year 2022, Okta projects revenue and loss per share to fall in the range of $1.243 – $1.250 billion and $0.77 – $0.74 per share, respectively. Consensus estimates for revenue and loss per share are pegged at $1.22 billion and $1.11 per share, respectively.

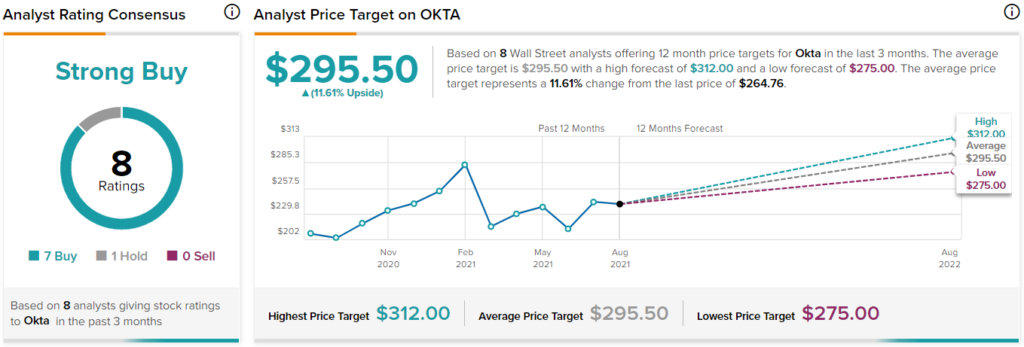

In response to Okta’s solid performance, Robert W. Baird analyst Jonathan Ruykhaver maintained a Hold rating on the stock but lifted the price target to $265 from $240. This implies that shares are fully valued at current levels.

The analyst notes that the Auth0 acquisition makes evaluation difficult despite the improved disclosures. However, he is encouraged by the organic performance during the quarter, including the acceleration of year-over-year sequential revenue growth.

Ruykhaver said, “Early commentary on Auth0 was positive; while we continue to see execution risk there, we do like the developer-friendly motion. This execution risk has us patient here, though we note that guidance looks quite achievable assuming management can minimize disruption.”

Overall, the stock commands a Strong Buy consensus rating based on 7 Buys and 1 Hold. The average Okta price target of $295.50 implies 11.6% upside potential to current levels. Shares have gained 14.8% over the past year.

Related News:

Five Below Falls 9% After-Hours on Mixed Q2 Results

CrowdStrike Dips 5% Despite Exceeding Q2 Expectations & Lifting Guidance

Anaplan Q2 Results Impress; Shares Surge 15% After-Hours