WASDE Update: Supply Expectations Edge Higher

In its World Agricultural Supply and Demand Estimates (WASDE) report, the USDA has raised its supply estimates for the 2021/22 marketing year on account of better weather in the US and elsewhere, and sees global ending stocks for corn, soybeans and wheat edge higher. The report was generally bearish, but the market was expecting this.

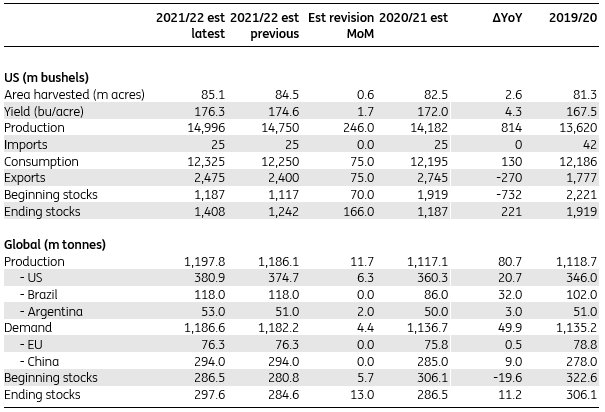

Corn supplies exceed expectations

As expected, the USDA increased its US corn yield estimates for 2021/22 to 176.3bu/acre compared to an earlier estimate of 174.6bu/acre. Combined with an increase in area, the USDA estimates US corn production to total around 15b bushels in 2021/22, compared to a previous estimate of 14.75b bushels and larger than the 14.18b bushels produced in 2020/21. Ahead of the WASDE, market expectations were for a 2021/22 production number of around 14.9b bushels. If the current estimate is realised, it would be the second largest US corn crop on record.

On the demand front, domestic corn consumption was revised up by around 75m bushels. The agency is now estimating that consumption totals 12.33b bushels. Export estimates were also revised higher by 75m bushels to 2.48b bushels; although this remains below the 2.75b bushels of exports estimated in 2020/21. Beginning stock estimates for 2021/22 were increased by around 70m bushels on account of lower demand in 2020/21. Larger beginning stocks, combined with expectations of additional supply, means the USDA sees the US corn market ending 2021/22 with inventories of around 1.41b bushels, up from a previous estimate of 1.24b bushels. The revised number is slightly higher than the roughly 1.3b bushels the market was expecting ahead of the release.

The global corn balance also saw loosening. The USDA increased its corn production estimate by around 11.7mt (6.3mt from the US and 5.4mt from elsewhere) for 2021/22 with major revisions coming from China and Argentina. Expectations for Chinese corn production were increased by around 5mt as a result of favourable weather in growing regions. While the Argentine crop estimate was increased by around 2mt. As a result, global corn inventory estimates at the end of 2021/22 were revised higher from 284.6mt to 297.6mt, while higher beginning stocks for 2021/22 also contributed to the increase. The market was expecting an inventory number of closer to 286mt. Therefore, clearly the report was more bearish than the market was anticipating.

Corn supply/demand estimates

USDA

Soybean inventory estimates revised higher

The USDA increased its US soybean yield estimates from 50bu/acre to 50.6bu/acre for 2021/22 due to improved weather. While, acreage estimates were revised down marginally for the year. As a result US soybean output is expected to edge up to 4.37b bushels, compared to a previous forecast of 4.34b bushels. The market was expecting a number of around 4.3b bushels. The USDA increased its soybean export estimate by around 35m bushels for the year; however, domestic consumption estimates were revised down by around 25m bushels leaving a net change in demand of around 10m bushels. As a result of these changes, along with higher beginning stocks, ending stocks for 2021/22 are estimated at 185m bushels, up from a previous estimtate of 155m bushels. The market had expected an ending stock number of around 190m bushels.

The USDA left its global soybean supply and demand estimates largely unchanged for 2021/22. However, ending stock estimates for 2020/21 were increased by around 2.3mt. Consequently, global ending stock estimates for 2021/22 were increased from 96.2mt to 98.9mt. The market was expecting a number of around 96.8mt. These changes are moderately bearish for the market.

Soybean supply/demand estimates

USDA

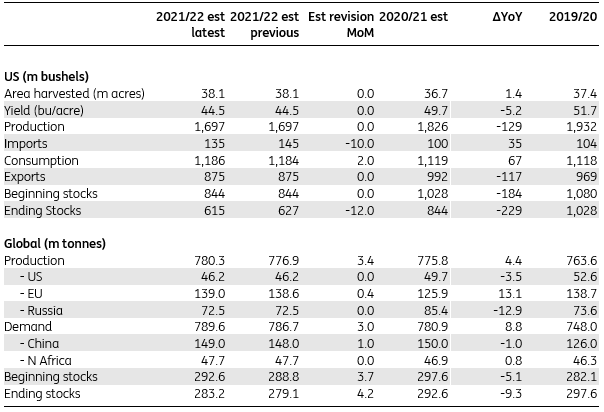

US wheat balance tightens further

The USDA once again revised down US wheat ending stock estimates in the domestic market for 2021/22. Although this time around it was due to lower than expected imports for the marketing year. The agency left its US wheat production estimate unchanged at 1.7b bushels; however, lowered import estimates by around 10m bushels. Domestic consumption and export estimates were also left largely unchanged at around 1.2b bushels and 0.88b bushels respectively. As a result wheat stock estimtes are estimated to end the 2021/22 season at around 615m bushels compared to a previous estimate of 627m bushels. The market had expected an ending stock number of around 616m bushels.

There were more changes to the global wheat balance. The USDA increased its production estimate by around 3.4mt for 2021/22 mostly on account of higher supplies from Australia (+1.5mt) and India (+1.5mt). However, this was mostly offset by an increase of around 3mt in global demand, which leaves the market balance largely unchanged with a supply shortfall of around 9.4mt for 2021/22. Global ending stocks for 2021/22 were revised up by 4.2mt to 283.2mt and this change was driven by revisions to opening stocks for the marketing year. In the lead up to the release the market was expecting ending stocks to be largely unchanged from last month at around 279mt.

While the report is supportive for the US domestic market, changes to the global balance are somewhat bearish.

Wheat supply/demand estimates

USDA

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more