Kunakorn Rassadornyindee/iStock via Getty Images

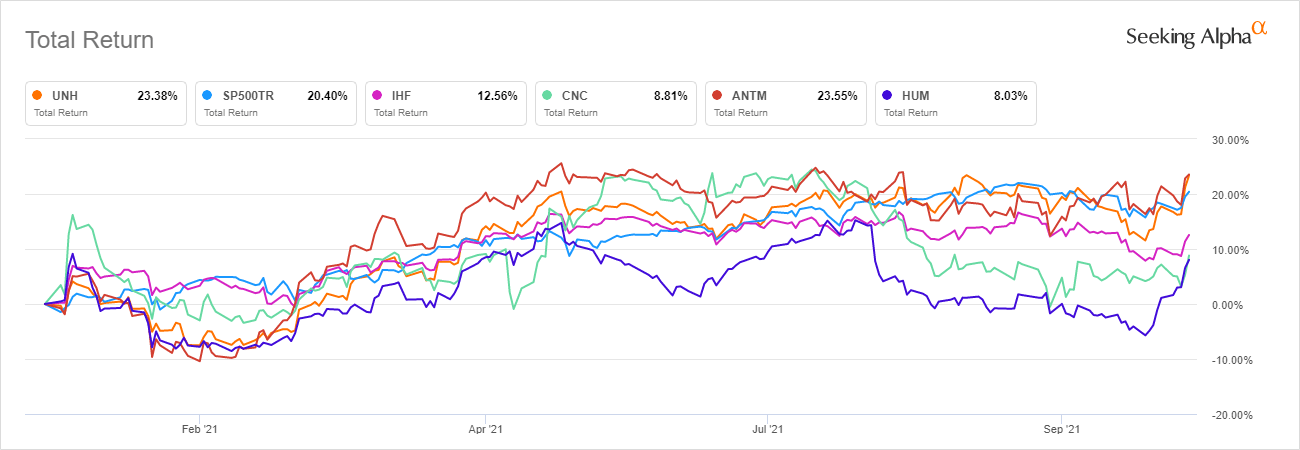

- The valuation disparities of managed care players have gained attention ahead of their earnings results, particularly, since industry bellwether UnitedHealth (NYSE:UNH) posted strong financials for Q3 2021 this week.

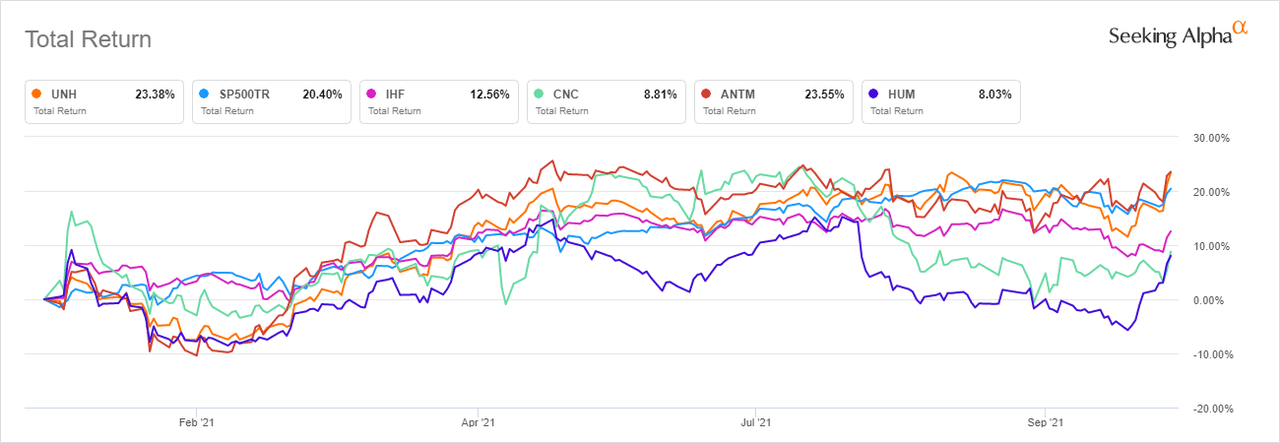

- Notwithstanding the YTD outperformance of the subsector, all three rivals, Anthem (NYSE:ANTM), Humana (NYSE:HUM), and Centene (NYSE:CNC), rose after UnitedHealth (UNH), the biggest in the Medicare advantage market, beat consensus and raised full-year guidance.

- With soft demand for elective procedures offsetting the additional costs of the pandemic care — the operator of UnitedHealthcare and pharmacy benefits unit, OptumHealth — shrugged off the COVID-19 impact on its bottom-line.

- “While the pandemic-related impacts remain difficult to predict, given the current trends, we would expect a lower unfavorable COVID impact than experienced in '21,” CFO John Rex said at the earnings call, noting that the revised guidance reflects an unchanged view on the pandemic.

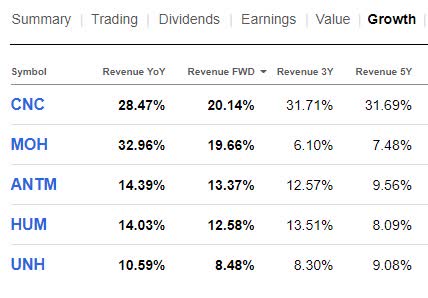

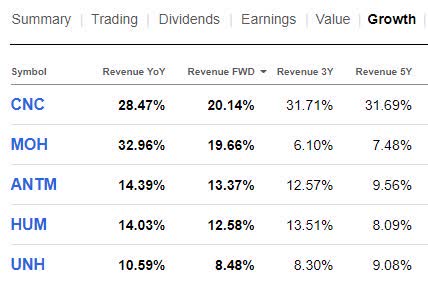

- Turning to peer performance up to Q2 2021, Centene (CNC) has recorded the best LTM revenue growth with a ~28% YoY growth compared to ~10% YoY growth of UnitedHealth (UNH) and ~14% YoY growth recorded by both Anthem (ANTM) and Humana (HUM).

- Despite the lowest forward earnings growth, Centene (CNC) — whose revenue is mainly dependent on Medicaid — is projected to beat rivals with its forward revenue growth, as indicated in the diagram above.

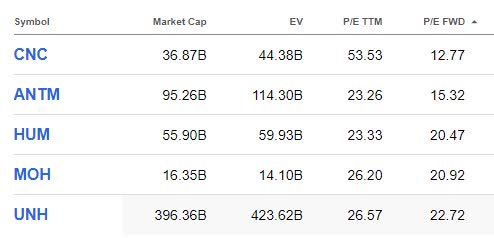

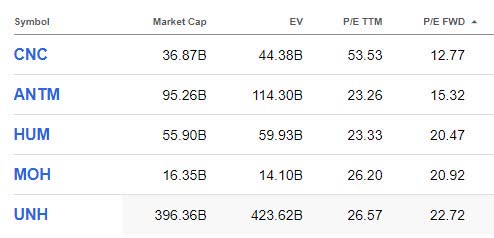

- And yet, St. Louis, Missouri-based company lags in valuation compared to rivals as well as its own historical performance.

- With a ~12.4% discount to the five-year average, Centene (CNC) trades at ~12.8x on a forward basis, compared to ~22.7x, ~20.4x, and ~15.3x forward earnings multiples of UnitedHealth (UNH), Humana (HUM), and Anthem (ANTM), respectively.

- Having the best Wall Street rating among peers, as shown below, Centene’s (CNC) ability to deliver will be in focus as the company prepares to report its Q3 2021 financials on Oct. 26 before the market opens.