Kirill Smyslov/iStock via Getty Images

- S&P Global Ratings boosts its credit rating on Tesla (TSLA +1.3%) to BB+.

- The ratings agency says the positive outlook reflects its view that Tesla's (NASDAQ:TSLA) free operating cash flow generation will remain positive more consistently, even as the company expands its global manufacturing footprint over the next 12 months.

- S&P calls it a key milestone that the automaker hit an annualized production run-rate of 1M units at the end of the third quarter.

- "EBITDA margins for Tesla remained strong so far this year; we expect margins to remain steady in 2022, despite some mix shift towards lower-priced vehicles i.e., Model 3 and Y relative to the higher-priced Model S and X. Going forward, we expect that higher fixed-cost absorption and cost reduction will continue to be offset by weaker mix, higher operating expenses (including supply-chain related), lower regulatory credit revenue, and higher commodity costs."

- S&P says it could consider an upgrade to an investment grade rating on Tesla if the company remains on a trajectory to sustain automotive EBITDA margins above 18% (excluding regulatory credits) as its Berlin and Austin production facilities come online.

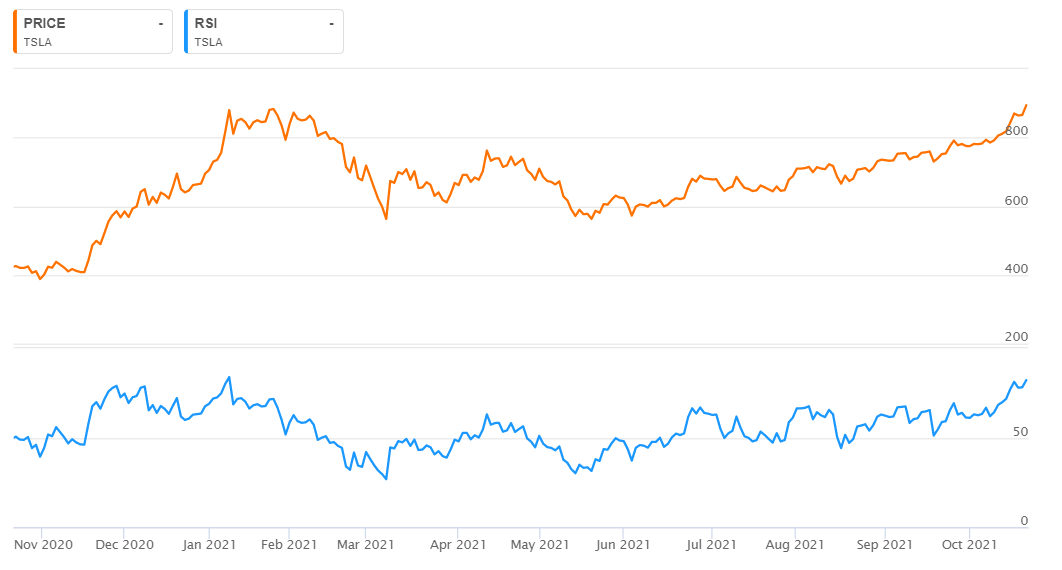

- Shares of Tesla (TSLA) traded at an all-time high of $910 earlier in today's session. The relative strength index on Tesla is at its highest level since January.