ChristianChan/iStock via Getty Images

- Goldman Sachs analyst Richard Ramsden sees M&A activity staying strong in 2022 and helping advisors and boutique investment banks, with strength also in equity capital markets and equities trading with "upside optionality in energy, Europe, and biotech."

- Sees the greatest risk of deceleration in fixed income, currencies & commodities ("FICC"), large-cap M&A, and SPACs.

- As a result of the 2022 outlook, Goldman upgraded Houlihan Lokey (NYSE:HLI) to Buy from Neutral and Moelis & Co. (NYSE:MC) to Neutral from Sell; downgrades Evercore (NYSE:EVR) to Neutral from Buy and removes it from Goldman's Americas Conviction List.

- Ramsden points out that firms diversifying revenue to other kinds of advisory beyond M&A — such as restructuring, capital markets, and shareholder activism — is making forecasting more difficult. As a result, only about 60% of advisory revenue can be explained by Dealogic data as of Q3 2021, down from 80% in 2013. That's led to the average earnings surprise at more than 2x the pre-pandemic period.

- Also sees lack of liquidity weighing on the group's valuation.

- The analyst sees Buy-rated Jefferies (NYSE:JEF) and Piper Sandler (NYSE:PIPR) well positioned to benefit from 2022 themes and continues to favor PJT Partners (NYSE:PJT) and Perella Weinberg Partners (NASDAQ:PWP) for company-specific growth potential that less tied to the cycle.

- More on the ratings actions: For Houlihan Lokey (HLI), the company's recent acquisition of GCA materially improves its near-term growth profile, shifting its business more toward M&A vs. restructuring, increases its banker base, and skews the business more toward areas that Ramsden expects to outperform within advisory.

- Goldman expects Moelis (MC) can boost its top line by 100 basis points in 2022 Y/Y on three areas expected to remain robust and accelerate — sponsors, healthcare, and energy.

- Evercore (EVR) offers a "compelling longer-term growth story," but has less medium-term revenue growth potential than many in its peer group as a larger proportion of its revenue comes from equities and ECM than its advisor peers and less relative exposure to areas of M&A where Goldman sees continued strength, particularly small and mid-cap and European M&A.

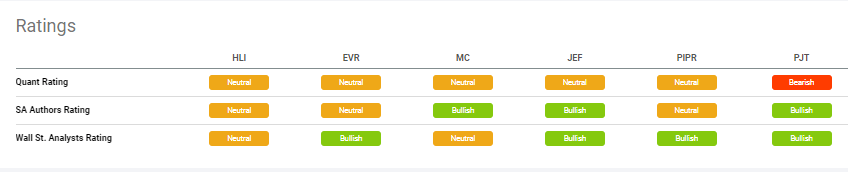

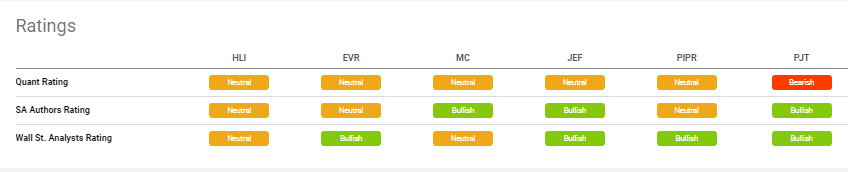

- Compare valuation, growth, profitability and performance stats of HLI, EVR, MC, JEF, PIPR, and PJT on this screen.

- SA contributor Opal Investment sees Houlihan Lokey's (HLI) premium valuation as a hurdle.