Market Briefing For Wednesday, May 18

Perceived risks are obvious which increasingly gets shorts nervous, as the S&P firms a bit. However it has not yet attacked key resistance levels at all.

Certainly Chairman Powell reiterating today that the Fed won't 'lay-off' hiking rates until they break inflation, sobered the market's slightly favorable tone, at the same time it didn't really derail the gradual upward progress.

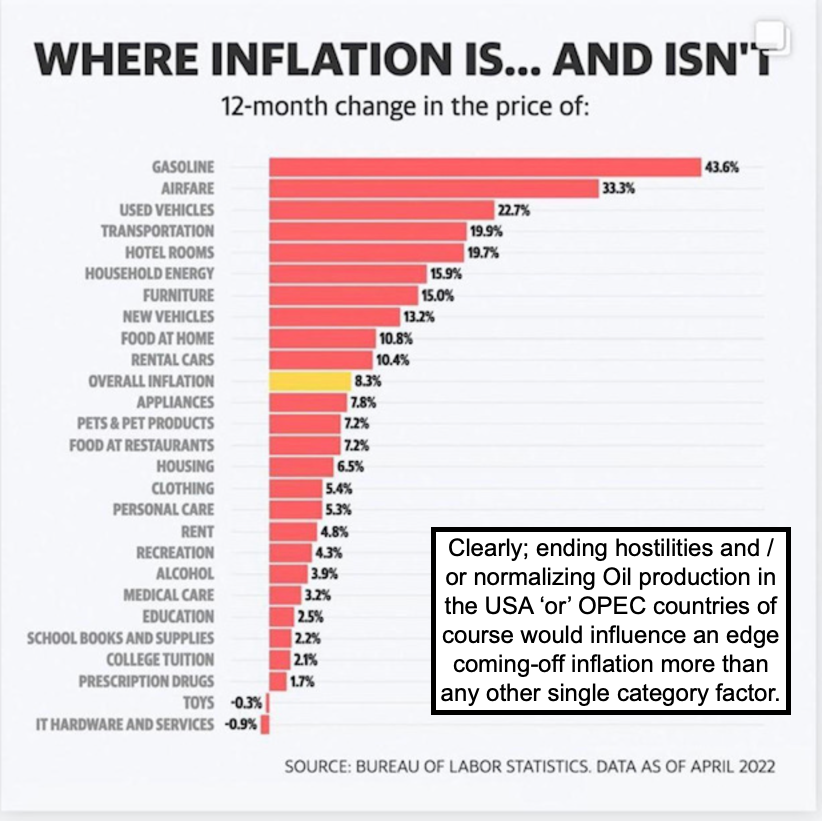

The actual inflationary pressures should impede a so-called robust economy, which adjusted for pricing, really isn't as exciting as some observe. Especially the case when it comes to average families trying to navigate the situation, as contrasted to more well-off families not particularly flustered by retail pricing of goods, gasoline, or even travel costs.

How the vacation costs aren't impacting anyone looking to take their families anywhere this Summer, is sort of puzzling. Airfares and hotels increasingly do not offer specials, and should be making a dent in budges for various trips, or even cause reconsideration of the length or trip frequencies. Perhaps coming.

There were a couple factors that 'do' help the backdrop. One is China clearly (or seemingly, as nobody knows what they'll say the next time) expressing the change-of-heart regarding technology regulations, and even easing shutdown COVID-related commerce-halts in many cities, most notable being Shanghai.

The other one is Washington, authorizing Chevron (CVX) to negotiate with the 'state owned oil company' in Caracas. Several weeks ago I noted a delegation very quietly having been sent to Venezuela, and now the Washington Post reports they are authorized to explore presumably oil sales to the USA, and how that relates to negotiating with the legally-elected Government versus the socialist Maduro regime, is hard to say.

The need for Oil (since Washington impeded a lot of U.S. exploration and the pipeline from Canada) is clear, as is the needs of Venezuela for revenue, after their absurd exploitation of their people or of course the horribly mismanaged operations and respect for Oil reserves. If anything, besides unhappy with the way Washington suppresses the domestic Oil & Gas industry, I am hopeful at least a bit, that Caracas gets an opening to move toward normal Government.

In-sum:

The market continues heading (grudgingly at times) toward what I've felt would be first (and perhaps key) resistance around S&P 4150-4200. For a week or so I've felt we'd get a relief rally given the near-universal negativity as well as a decline that entered the S&P 3800's, without too much drama (knew that would be tough since so many stocks had already crashed), either way it was setting-up for what we've got.

The Fed continues to wax in unfriendly ways, which makes it tricky, but we're still inclined to be slightly favorable for higher prices, especially is something else in a sense 'gives', which for example was China's technology policy shift (back to a favorable light for the moment) that also helped today. Given how many continue to cite doom & gloom, we believe that worst is behind for most smaller stocks (where business models are intact and viable) while it varies in other sectors, with Retail still heavily impacted by profit margins and so on. If a decline in Diesel fuel and some movement towards a ceasefire in Ukraine is also forthcoming, then odds last week being an important S&P low, increase.

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more