Oracle (NYSE: ORCL) is one of the biggest names around in computer technology, offering up an array of cloud-based applications as well as a complete cloud infrastructure operation. Taking a look at Oracle’s overall situation and what the company has got going on right now should be encouraging to Oracle investors. In fact, I’m bullish on Oracle right now, thanks to a series of factors.

After market close today, the company released earnings data and offered up a look at how the last quarter went. The results for Oracle proved a bit mixed. Earnings per share—on a non-GAAP basis—came in at $1.03 per share. That’s a slight miss against the TipRanks consensus, which looked for $1.08 per share. Revenue, however, was a bit better. Total revenue for the first quarter was $11.4 billion, in line with analysts’ expectations but higher than the company’s guidance.

Oracle’s substantial growth in revenue can be immediately traced to its acquisition of Cerner, a medical records company. However, that’s not the only thing giving Oracle’s growth a shot in the arm.

With Cerner, revenue was up 23%. Without, it was up 8%. The news was good enough for Oracle to declare a cash dividend of $0.32 per share, with a payment date of October 25.

The last 12 months for Oracle shares started off well, then started a multi-month drop that only recently turned around. Last year at this time, Oracle shares sold around $88 before reaching their 52-week high of $105.06. Now, the company finds itself in the $77 – $78 range.

Is Oracle Stock a Buy or Sell?

Turning to Wall Street, Oracle has a Moderate Buy consensus rating. That’s based on eight Buys, 11 Holds, and one Sell assigned in the past three months. The average Oracle price target of $89.33 implies 15.89% upside potential.

Analyst price targets range from a low of $70 per share to a high of $115 per share.

Investor Sentiment Is Looking Up – for the Most Part

Immediately, there’s one major point in Oracle’s favor. Oracle currently has a Smart Score of 9 out of 10 on TipRanks. That puts it at the second-highest level of “outperform.” That makes Oracle shares much more likely to perform better than the broader market.

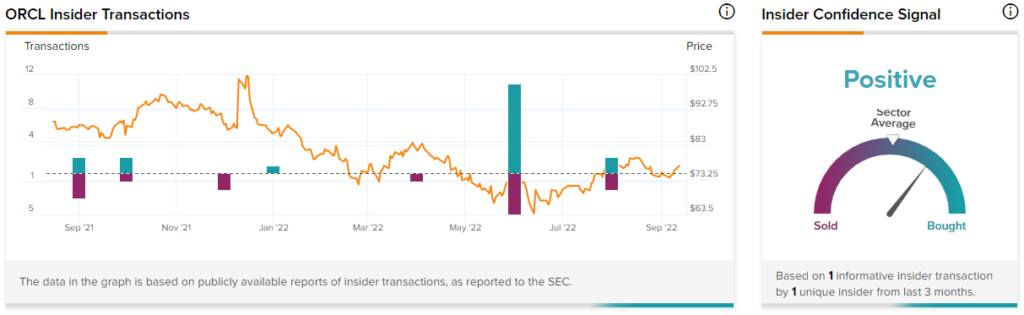

Better still for Oracle is its recent figures on insider trading. Oracle insiders have spent the last few months buying Oracle stock at a pretty frantic pace. In just the last three months, Oracle insiders bought over $208 million in shares. The biggest such contributor was Larry Ellison‘s purchase of $208.04 million in shares.

However, it’s worth noting that, just before that, CEO/Director Safra Catz sold over $204.4 million worth of shares in the form of an Uninformative Sell. Catz then staged a second uninformative sale for just over $135.5 million just after Ellison’s purchase.

Looking at the aggregate is even better for Oracle. The last 12 months feature quite a bit more buying than selling, with 18 Buys and 14 Sells taking place. While most of these transactions are still considered uninformative, there’s still quite a bit of buying going on against selling activity.

Product Line Diversification Will Prove Oracle’s Saving Grace

Granted, Oracle isn’t likely to be a household word. Most people will have little contact with Oracle systems. Their jobs, however, likely will have much more dependence on Oracle and its systems. Thus, it’s a good thing that Oracle seems to be moving along like a house afire, even in this economy. Several key Oracle-related moves have emerged in recent days. Accenture (NYSE: ACN), for example, recently acquired the supply-chain management operation Inspirage in a bid to step up its Oracle-focused business.

Inspirage’s 710 employees will all be Accenture employees now and will be tasked with helping businesses implement Oracle products like the Oracle Autonomous Cloud.

Clearly, Accenture is looking for Oracle to continue to produce in a big way. After all, Accenture and Oracle have been closely linked for the last 30 years. Just a week ago, analysts expected Oracle to release numbers that would ultimately lead it past Google Cloud as the fastest-growing provider of cloud systems.

When you beat Google in anything, you’ve clearly done something right. Even being in a position to challenge Google is a real step forward. One of the biggest steps to getting to such a position is to have a solid product line to work with.

TechRepublic recently staged a head-to-head comparison between Oracle and Workday (NASDAQ: WDAY) and found the two comparatively similar. However, Oracle had an edge in performance management and international payroll, which makes it well-suited to large corporate needs. Large corporations are the most likely to survive the upcoming economic downturn. That puts their suppliers, like Oracle, in a better position.

Throw in the sheer diversity of Oracle’s product range, and the picture only improves. A presence in healthcare, government, and education, and in a panoply of other market verticals, helps ensure that there will be sales somewhere.

Conclusion: ORCL Stock Presents a Solid Opportunity

There’s a reason to be bullish about Oracle. The first of these is its overall price level; the company is trading only slightly over its lowest price targets. That suggests a decent entry point. Sure, it’s not as good as it was back in June, but there is still clearly plenty of upside potential left to go.

A look at the insider trading figures makes it clear that insiders were waiting for a bottom to buy in big – and buy in big they did. Safra Catz’s frantic sell-off might be a little concerning, but the sheer number of insider purchases makes this worth a second look. Throw in its close connections to larger businesses, and that improves its likelihood of surviving an economic downturn.

Oracle is in a good position, going forward. It’s become sufficiently big to challenge Google itself, and that’s no mean feat. Combining it with a decent price point makes it that much more compelling, and that’s why I’m bullish on Oracle.